Filed by Wildfire New PubCo, Inc. pursuant to Rule 425 under the Securities Act of 1933 and deemed filed pursuant to Rule 14a-12 under the Securities Exchange Act of 1934 Subject Company: Jack Creek Investment Corp. Commission File No.: 001-39602 Date: December 29, 2022 Bridger Aerospace Investor Presentation December 2022

Important Disclaimers Basis of Presentation This Presentation (this “Presentation”) is provided for informational purposes only and has been prepared to assist interested parties in making their own evaluation with respect to a business combination between Bridger Aerospace Group Holdings, LLC (“Bridger”, “Bridger Aerospace” or the “Company”) and Jack Creek Investment Corp. (“Jack Creek” or “JCIC”) and related transactions (the “Business Combination”) and for no other purpose. By accepting, reviewing or reading this Presentation, you will be deemed to have agreed to the obligations and restrictions set out below. No Offer or Solicitation This Presentation and any oral statements made in connection with this Presentation do not constitute an offer to sell, or a solicitation of an offer to buy, or a recommendation to purchase, any securities in any jurisdiction, or the solicitation of any vote, consent or approval in any jurisdiction in connection with the Business Combination or any related transactions, nor shall there be any sale, issuance or transfer of any securities in any jurisdiction where, or to any person to whom, such offer, solicitation or sale may be unlawful under the laws of such jurisdiction. This Presentation does not constitute either advice or a recommendation regarding any securities. No offering of securities shall be made except by means of a prospectus meeting the requirements of the Securities Act of 1933, as amended, or an exemption therefrom. Industry and Market Data No representations or warranties, express, implied or statutory are given in, or in respect of, this Presentation, and no person may rely on the information contained in this Presentation. To the fullest extent permitted by law, in no circumstances will Bridger or Jack Creek or any of their respective subsidiaries, stockholders, affiliates, representatives, partners, directors, officers, employees, advisers or agents be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of this Presentation, its contents, its omissions, reliance on the information contained within it or on opinions communicated in relation thereto or otherwise arising in connection therewith. This Presentation discusses trends and markets that Bridger’s leadership team believes will impact the development and success of Bridger based on its current understanding of the marketplace. Industry and market data used in this Presentation have been obtained from third-party industry publications and sources as well as from research reports prepared for other purposes. Neither Jack Creek nor Bridger has independently verified the data obtained from these sources and cannot assure you of the reasonableness of any assumptions used by these sources or the data’s accuracy or completeness. Any data on past performance or modeling contained herein is not an indication as to future performance. This data is subject to change. Recipients of this Presentation are not to construe its contents, or any prior or subsequent communications from or with Jack Creek, Bridger or their respective representatives as investment, legal or tax advice. The Recipient should seek independent third party legal, regulatory, accounting and/or tax advice regarding this Presentation. In addition, this Presentation does not purport to be all-inclusive or to contain all of the information that may be required to make a full analysis of Bridger or the Business Combination. Recipients of this Presentation should each make their own evaluation of Bridger and of the relevance and adequacy of the information and should make such other investigations as they deem necessary. Jack Creek and Bridger assume no obligation to update the information in this Presentation. 2

Important Disclaimers Forward Looking Statements Certain statements included in this Presentation are not historical facts but are forward-looking statements, including for purposes of the safe harbor provisions under the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements generally are accompanied by words such as “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “should,” “would,” “plan,” “project,” “forecast,” “predict,” “potential,” “seem,” “seek,” “future,” “outlook,” “target,” and similar expressions that predict or indicate future events or trends or that are not statements of historical matters, but the absence of these words does not mean that a statement is not forward- looking. These forward-looking statements include, but are not limited to, (1) references with respect to the anticipated benefits of the Business Combination and anticipated closing timing; (2) the sources and uses of cash of the Business Combination; (3) the anticipated capitalization and enterprise value of the combined company following the consummation of the Business Combination; (4) current and future potential commercial and customer relationships; and (5) anticipated investments in additional aircraft, capital resource, and research and development and the effect of these investments. These statements are based on various assumptions, whether or not identified in this Presentation, and on the current expectations of JCIC’s and Bridger’s management and are not predictions of actual performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond the control of JCIC and Bridger. These forward-looking statements are subject to a number of risks and uncertainties, including: changes in domestic and foreign business, market, financial, political and legal conditions; the inability of the parties to successfully or timely consummate the Business Combination, including the risk that any required stockholder or regulatory approvals are not obtained, are delayed or are subject to unanticipated conditions that could adversely affect the combined company or the expected benefits of the Business Combination is not obtained; failure to realize the anticipated benefits of the Business Combination; risks relating to the uncertainty of the projected financial information with respect to Bridger; Bridger’s ability to successfully and timely develop, sell and expand its technology and products, and otherwise implement its growth strategy; risks relating to Bridger’s operations and business, including information technology and cybersecurity risks, loss of requisite licenses, flight safety risks, loss of key customers and deterioration in relationships between Bridger and its employees; risks related to increased competition; risks relating to potential disruption of current plans, operations and infrastructure of Bridger as a result of the announcement and consummation of the Business Combination; risks that Bridger is unable to secure or protect its intellectual property; risks that the post-combination company experiences difficulties managing its growth and expanding operations; the ability to compete with existing or new companies that could cause downward pressure on prices, fewer customer orders, reduced margins, the inability to take advantage of new business opportunities, and the loss of market share; the amount of redemption requests made by JCIC’s shareholders; the impact of the COVID-19 pandemic; the ability to successfully select, execute or integrate future acquisitions into the business, which could result in material adverse effects to operations and financial conditions; and those factors discussed in the Appendix to this Presentation and set forth in the section entitled “Risk Factors” and “Special Note Regarding Forward‐Looking Statements” in Jack Creek’s Quarterly Report on Form 10‐Q for the quarter ended September 30, 2022, Jack Creek's Annual Report on Form 10‐K for the year ended December 31, 2021, and the registration statement on Form S-4, as amended, initially filed on August 12, 2022 by Wildfire New PubCo, Inc., a wholly-owned subsidiary of Jack Creek (“New PubCo”), and declared effective by the U.S. Securities and Exchange Commission (the SEC ) on December 16, 2022 (the Registration Statement ), as well as in those documents that Jack Creek and New PubCo, has filed, or will file, with the SEC. If any of these risks materialize or our assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. The risks and uncertainties above are not exhaustive, and there may be additional risks that neither JCIC nor Bridger presently know or that JCIC and Bridger currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In addition, forward looking statements reflect JCIC’s and Bridger’s expectations, plans or forecasts of future events and views as of the date of this Presentation. JCIC and Bridger anticipate that subsequent events and developments will cause JCIC’s and Bridger’s assessments to change. However, while JCIC and Bridger may elect to update these forward-looking statements at some point in the future, JCIC and Bridger specifically disclaim any obligation to do so. These forward-looking statements should not be relied upon as representing JCIC’s and Bridger’s assessments as of any date subsequent to the date of this Presentation. Accordingly, undue reliance should not be placed upon the forward-looking statements. 3

Important Disclaimers Trademarks Jack Creek and Bridger own or have rights to various trademarks, service marks and trade names that they use in connection with the operation of their respective businesses. This Presentation also contains trademarks, service marks, trade names and copyrights of third parties, which are the property of their respective owners. The use or display of third parties’ trademarks, service marks, trade names or products in this Presentation is not intended to, and does not imply, a relationship with Jack Creek or Bridger, an endorsement or sponsorship by or of Jack Creek or Bridger, or a guarantee the Bridger or Jack Creek will work or will continue to work with such third parties. Solely for convenience, the trademarks, service marks, trade names and copyrights referred to in this Presentation may appear without the TM, SM, ® or © symbols, but such references are not intended to indicate, in any way, that Jack Creek, Bridger, or the any third-party will not assert, to the fullest extent under applicable law, their rights or the right of the applicable licensor to these trademarks, service marks, trade names and copyrights. Non-GAAP Financial Measures Some of the financial information and data contained in this Presentation, such as Adjusted EBITDA (“Adj. EBITDA”), Adjusted EBITDA margin (“Adj. EBITDA margin”), Adjusted EBITDA per Scooper, Growth Capital Expenditures (“Growth CapEx”), Maintenance and Miscellaneous Capital Expenditures (“Maintenance and Miscellaneous CapEx”) and Free Cash Flow, have not been prepared in accordance with United States generally accepted accounting principles (“GAAP”). Adjusted EBITDA is defined as net earnings (loss) before interest expense, income tax expense (benefit), depreciation and amortization, as adjusted to exclude non-cash items or certain transactions that management does not believe are indicative of ongoing Company operating performance, which historically have included losses on disposals of assets, legal fees related to financing transactions, offering costs, loss on extinguishment of debt, bonuses to executives and international spend. Growth Capital Expenditures is defined as capital expenditures relating to the acquisition of new aircraft and facilities (other than replacement aircraft and facilities), and Maintenance and Miscellaneous Capital Expenditures is defined as Capital Expenditures less Growth Capital Expenditures. Free Cash Flow is defined as Adjusted EBITDA less Maintenance and Miscellaneous Capital Expenditures. Adjusted EBITDA per Scooper is defined as the average net earnings (loss) per Super Scooper before interest expense, income tax expense (benefit), depreciation and amortization. These non-GAAP financial measures, and other measures that are calculated using such non-GAAP measures, are an addition to, and not a substitute for or superior to, measures of financial performance prepared in accordance with GAAP and should not be considered as an alternative to revenue, operating income, profit before tax, net income or any other performance measures derived in accordance with GAAP. A reconciliation of the projected non-GAAP financial measures has not been provided and is unable to be provided without unreasonable effort because certain items excluded from these non-GAAP financial measures cannot be reasonably calculated or predicted at this time. For the same reasons, Bridger is unable to address the probable significance of the unavailable information, which could be material to future results. Jack Creek and Bridger believe these non-GAAP measures of financial results, including on a forward-looking basis, provide useful information to management and investors regarding certain financial and business trends relating to Bridger’s financial condition and results of operations. Bridger’s management uses these non-GAAP measures for trend analyses, for purposes of determining management incentive compensation, and for budgeting and planning purposes. Jack Creek and Bridger believe that the use of these non-GAAP financial measures provides an additional tool for investors to use in evaluating projected operating results and trends in and in comparing Bridger’s financial measures with other similar companies, many of which present similar non-GAAP financial measures to investors. However, there are a number of limitations related to the use of these non-GAAP measures and their nearest GAAP equivalents. For example, other companies may calculate non-GAAP measures differently, or may use other measures to calculate their financial performance, and therefore Bridger’s non-GAAP measures may not be directly comparable to similarly titled measures of other companies. See the Appendix for reconciliations of these non-GAAP financial measures to the most directly comparable GAAP measures. Use of Projections This Presentation contains projected financial information with respect to Bridger, namely revenue, gross profit, Adjusted EBITDA, Adjusted EBITDA margin, Adjusted EBITDA per Scooper, Growth Capital Expenditures, Maintenance and Miscellaneous Capital Expenditures, and Free Cash Flow for 2022-2023. Such projected financial information constitutes forward-looking information for illustrative purposes only and should not be relied upon as necessarily being indicative of future results. The projections, estimates and targets in this Presentation are forward-looking statements that are based on assumptions that are inherently subject to significant uncertainties and contingencies, many of which are beyond Jack Creek’s and Bridger’s control. See “Forward-Looking Statements” above. The assumptions and estimates underlying the projected, expected or target results are inherently uncertain and are subject to a wide variety of significant business, weather, economic, regulatory, competitive, technological, and other risks and uncertainties that could cause actual results to differ materially from those contained in such projections, estimates and targets. The inclusion of projections, estimates and targets in this Presentation should not be regarded as an indication that Jack Creek and Bridger, or their representatives, considered or consider the financial projections, estimates and targets to be a reliable prediction of future events. Neither the independent auditors of Jack Creek nor the independent registered public accounting firm of Bridger has audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this Presentation, and accordingly, neither of them expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this Presentation. 4

Important Disclaimers Important Information for Investors and Stockholders The Business Combination will be submitted to shareholders of Jack Creek for their consideration and approval at a special meeting of shareholders. Jack Creek and Bridger prepared the Registration Statement, which includes the definitive proxy statement that has been distributed to Jack Creek’s shareholders in connection with Jack Creek’s solicitation for proxies for the vote by Jack Creek’s shareholders in connection with the Business Combination and other matters as described in the Registration Statement, as well as the prospectus relating to the offer of the securities to be issued to Jack Creek’s shareholders and certain of Bridger’s equityholders in connection with the completion of the Business Combination. Jack Creek has mailed the definitive proxy statement and other relevant documents to its shareholders as of the record date established for voting on the Business Combination. Jack Creek’s shareholders and other interested persons are advised to read the definitive proxy statement/prospectus in connection with Jack Creek’s solicitation of proxies for its special meeting of shareholders to be held to approve, among other things, the Business Combination, because it contains important information about Jack Creek, Bridger and the Business Combination. Shareholders may also obtain a copy of the definitive proxy statement, as well as other documents filed with the SEC regarding the Business Combination and other documents filed with the SEC by Jack Creek, without charge, at the SEC’s website located at www.sec.gov. Copies of these filings may be obtained free of charge on Jack Creek’s “Investor Relations” website at https://www.jackcreekinvestmentcorp.com/ or by directing a request to KSH Capital LP, Attention: Lauren Ores, 386 Park Avenue South, FL 20, New York, NY 10016. Jack Creek and Bridger and their respective directors and executive officers, under SEC rules, may be deemed to be participants in the solicitation of proxies of Jack Creek’s shareholders in connection with the Business Combination. Investors and security holders may obtain more detailed information regarding Jack Creek’s directors and executive officers in Jack Creek’s filings with the SEC, including Jack Creek’s Annual Report on Form 10-K filed with the SEC on March 21, 2022. Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of proxies to Jack Creek’s shareholders in connection with the Business Combination, including a description of their direct and indirect interests, which may, in some cases, be different than those of Jack Creek’s shareholders generally, is set forth in the Registration Statement. Shareholders, potential investors and other interested persons should read the Registration Statement carefully before making any voting or investment decisions. This Presentation is not a substitute for the Registration Statement or for any other document that Jack Creek or New PubCo has filed and may file with the SEC in connection with the Business Combination. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain free copies of other documents filed with the SEC by Jack Creek and New PubCo through the website maintained by the SEC at http://www.sec.gov. Changes and Additional Information in Connection with SEC Filings The information in this Presentation has not been reviewed by the SEC and certain information, such as financial measures referenced herein, may not comply in certain respects with SEC rules. As a result, the information in the Registration Statement may differ from this Presentation to comply with SEC rules. The Registration Statement includes substantial additional information about Bridger and Jack Creek not contained in this Presentation. The information in the Registration Statement updates and supersedes the information presented in this Presentation. INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY NOR HAS ANY AUTHORITY PASSED UPON OR ENDORSED THE MERITS OF THE BUSINESS COMBINATION OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE. 5

Table of Contents Table of Contents Executive Summary 7 The Bridger Solution 18 Financial Overview 26 Transaction Details and Benchmarking 32 Appendix 35 6

Executive Summary

Agenda Presenters The Bridger Solution 1 Financial Overview 2 Tim Sheehy McAndrew Rudisill Chief Investment Officer Chief Executive Officer, Founder & Director & Director Transaction Details and Benchmarking 3 Jeff Kelter Robert Savage Chief Executive Officer Executive Chairman 8

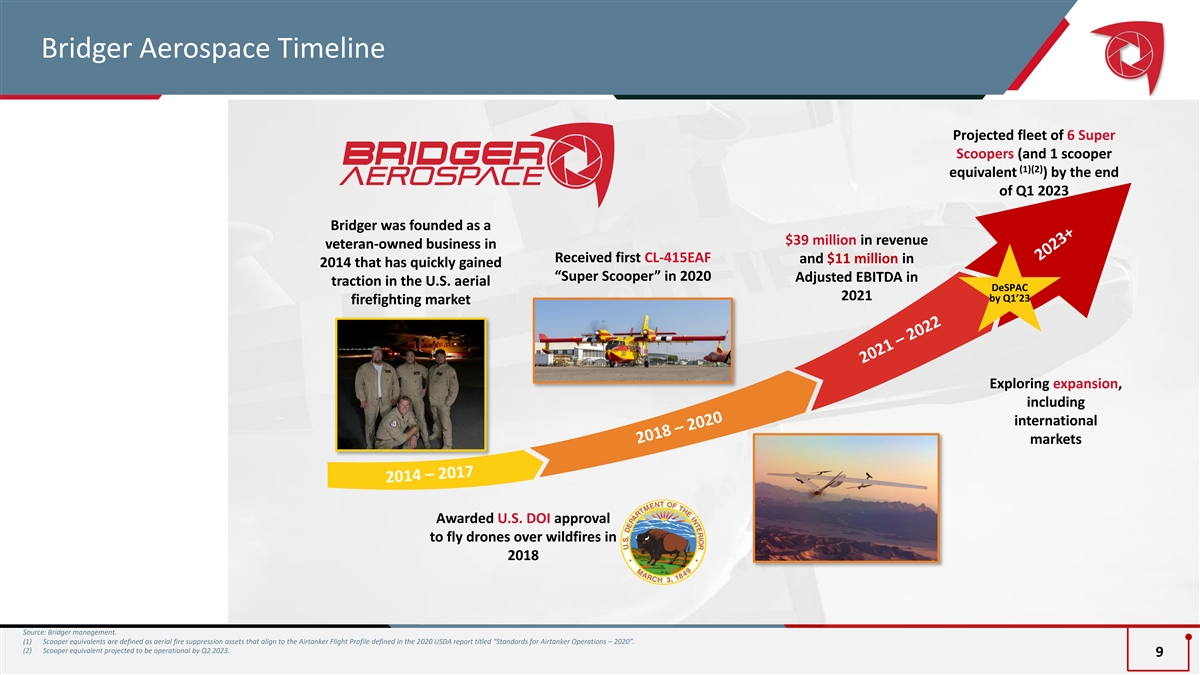

Bridger Aerospace Timeline Projected fleet of 6 Super Scoopers (and 1 scooper (1)(2) equivalent ) by the end of Q1 2023 Bridger was founded as a $39 million in revenue veteran-owned business in Received first CL-415EAF and $11 million in 2014 that has quickly gained “Super Scooper” in 2020 Adjusted EBITDA in traction in the U.S. aerial DeSPAC 2021 by Q1’23 firefighting market Exploring expansion, including international markets Awarded U.S. DOI approval to fly drones over wildfires in 2018 Source: Bridger management. (1) Scooper equivalents are defined as aerial fire suppression assets that align to the Airtanker Flight Profile defined in the 2020 USDA report titled “Standards for Airtanker Operations – 2020”. (2) Scooper equivalent projected to be operational by Q2 2023. 9

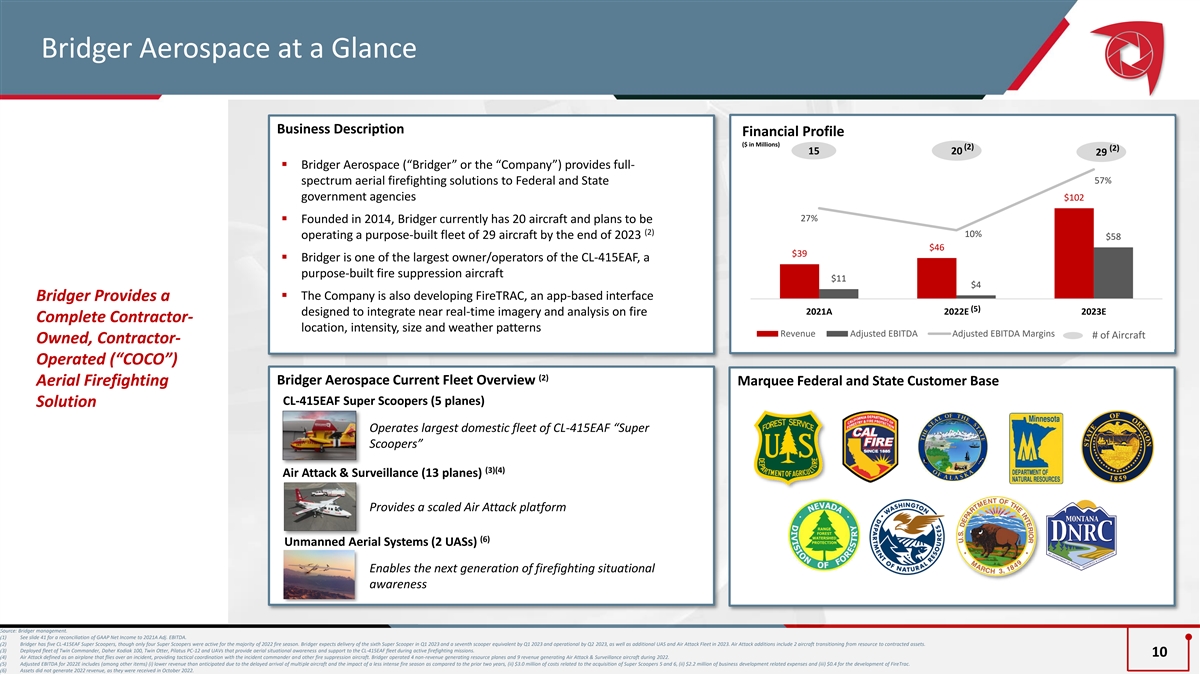

Bridger Aerospace at a Glance Business Description Financial Profile ($ in Millions) (2) (2) 15 20 29 ▪ Bridger Aerospace (“Bridger” or the “Company”) provides full- 57% spectrum aerial firefighting solutions to Federal and State government agencies $102 27% ▪ Founded in 2014, Bridger currently has 20 aircraft and plans to be (2) 10% operating a purpose-built fleet of 29 aircraft by the end of 2023 $58 $46 $39 ▪ Bridger is one of the largest owner/operators of the CL-415EAF, a purpose-built fire suppression aircraft $11 $4 ▪ The Company is also developing FireTRAC, an app-based interface Bridger Provides a (5) 2021A 2022E 2023E designed to integrate near real-time imagery and analysis on fire Complete Contractor- location, intensity, size and weather patterns Revenue Adjusted EBITDA Adjusted EBITDA Margins # of Aircraft Owned, Contractor- Operated (“COCO”) (2) Bridger Aerospace Current Fleet Overview Aerial Firefighting Marquee Federal and State Customer Base CL-415EAF Super Scoopers (5 planes) Solution Operates largest domestic fleet of CL-415EAF “Super Scoopers” (3)(4) Air Attack & Surveillance (13 planes) Provides a scaled Air Attack platform (6) Unmanned Aerial Systems (2 UASs) Enables the next generation of firefighting situational awareness Source: Bridger management. (1) See slide 41 for a reconciliation of GAAP Net Income to 2021A Adj. EBITDA. (2) Bridger has five CL-415EAF Super Scoopers, though only four Super Scoopers were active for the majority of 2022 fire season. Bridger expects delivery of the sixth Super Scooper in Q1 2023 and a seventh scooper equivalent by Q1 2023 and operational by Q2 2023, as well as additional UAS and Air Attack Fleet in 2023. Air Attack additions include 2 aircraft transitioning from resource to contracted assets. (3) Deployed fleet of Twin Commander, Daher Kodiak 100, Twin Otter, Pilatus PC-12 and UAVs that provide aerial situational awareness and support to the CL-415EAF fleet during active firefighting missions. 10 (4) Air Attack defined as an airplane that flies over an incident, providing tactical coordination with the incident commander and other fire suppression aircraft. Bridger operated 4 non-revenue generating resource planes and 9 revenue generating Air Attack & Surveillance aircraft during 2022. (5) Adjusted EBITDA for 2022E includes (among other items) (i) lower revenue than anticipated due to the delayed arrival of multiple aircraft and the impact of a less intense fire season as compared to the prior two years, (ii) $3.0 million of costs related to the acquisition of Super Scoopers 5 and 6, (ii) $2.2 million of business development related expenses and (iii) $0.4 for the development of FireTrac. (6) Assets did not generate 2022 revenue, as they were received in October 2022.

Bridger’s Critical Mission Bridger’s Mission is to Fight Wildfires that Cause Hundreds of Billions of Dollars of Economic Damage and Emit Hundreds of Millions of Metric Tons of CO into the 2 Mitigate economic Minimize Directly attack CO Atmosphere Annually 2 loss as wildfire environmental harm emissions to combat severity, frequency and through eco-friendly climate change damage rises and sustainable firefighting methods Source: AccuWeather, Bankrate, ABC10 and CalMatters. 11

Entrepreneurial Management Team With a Track Record of Success Bridger is Led by an Experienced Executive Team with a Track Record of McAndrew Rudisil Successfully Tim Sheehy Eric Gerratt James Muchmore Chief Investment Officer Chief Executive Officer Chief Financial Officer Chief Legal Officer Developing Businesses ◼ Founded Bridger Aerospace ◼ Joined Bridger Aerospace in ◼ Joined Bridger Aerospace in ◼ Joined Bridger Aerospace in in 2014 2022 as CFO 2017 as CIO 2017 as Chief Legal Officer ◼ Former Navy SEAL and ◼ Former CFO & Treasurer of US ◼ Extensive experience ◼ Extensive securities certified pilot Ecology successfully building and regulation, litigation and growing businesses aviation law experience ◼ Former CEO and Founder of ◼ Extensive experience in public Ascent Vision Technologies company financial reporting and accounting 12

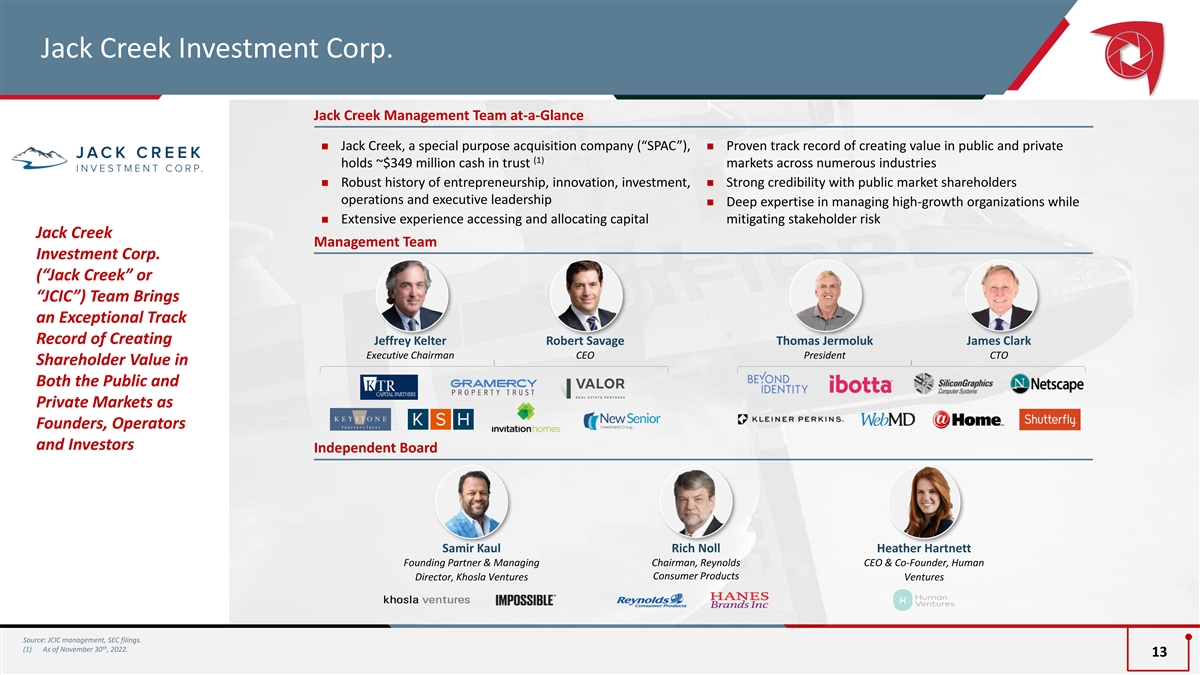

Jack Creek Investment Corp. Jack Creek Management Team at-a-Glance ◼ Jack Creek, a special purpose acquisition company (“SPAC”), ◼ Proven track record of creating value in public and private (1) holds ~$349 million cash in trust markets across numerous industries ◼ Robust history of entrepreneurship, innovation, investment, ◼ Strong credibility with public market shareholders operations and executive leadership ◼ Deep expertise in managing high-growth organizations while ◼ Extensive experience accessing and allocating capital mitigating stakeholder risk Jack Creek Management Team Investment Corp. (“Jack Creek” or “JCIC”) Team Brings an Exceptional Track Record of Creating Jeffrey Kelter Robert Savage Thomas Jermoluk James Clark Executive Chairman CEO President CTO Shareholder Value in Both the Public and Private Markets as Founders, Operators and Investors Independent Board Samir Kaul Rich Noll Heather Hartnett Founding Partner & Managing Chairman, Reynolds CEO & Co-Founder, Human Consumer Products Director, Khosla Ventures Ventures Source: JCIC management, SEC filings. th (1) As of November 30 , 2022. 13

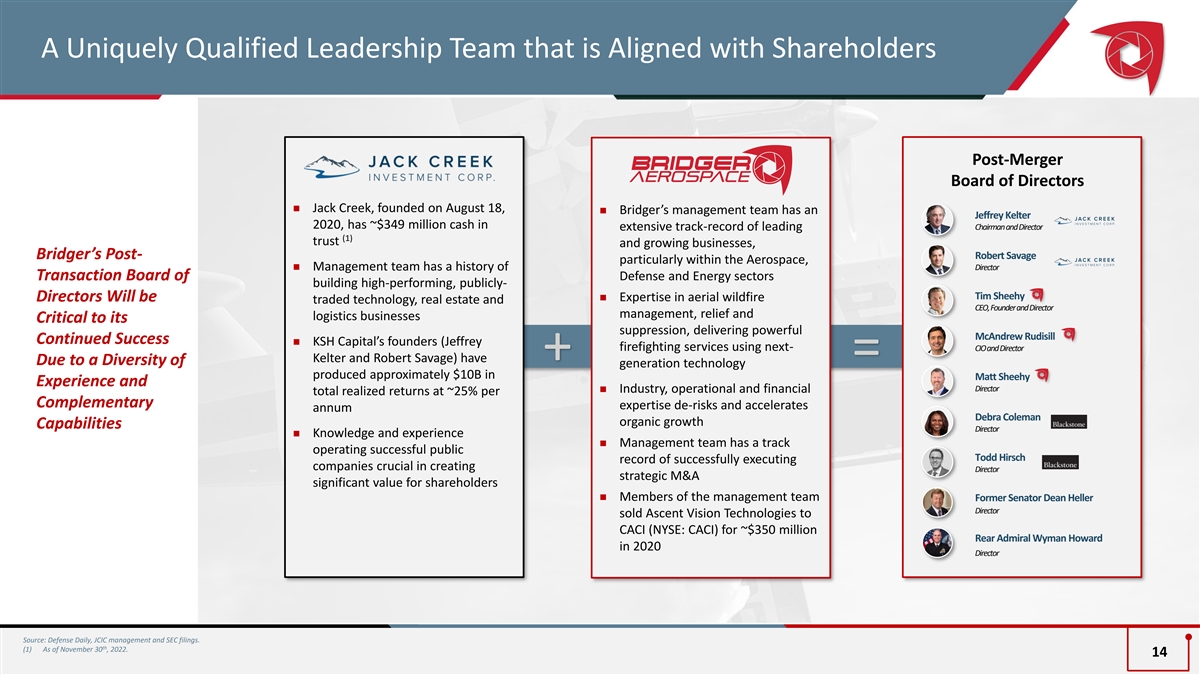

A Uniquely Qualified Leadership Team that is Aligned with Shareholders Post-Merger Board of Directors ◼ Jack Creek, founded on August 18, ◼ Bridger’s management team has an Jeffrey Kelter 2020, has ~$349 million cash in Chairman and Director extensive track-record of leading (1) trust and growing businesses, Bridger’s Post- Robert Savage particularly within the Aerospace, ◼ Management team has a history of Director Transaction Board of Defense and Energy sectors building high-performing, publicly- Tim Sheehy ◼ Expertise in aerial wildfire Directors Will be traded technology, real estate and CEO, Founder and Director management, relief and logistics businesses Critical to its suppression, delivering powerful McAndrew Rudisill Continued Success ◼ KSH Capital’s founders (Jeffrey firefighting services using next- CIO and Director Kelter and Robert Savage) have + = Due to a Diversity of generation technology produced approximately $10B in Matt Sheehy Experience and Director ◼ Industry, operational and financial total realized returns at ~25% per Complementary expertise de-risks and accelerates annum Debra Coleman organic growth Capabilities Director ◼ Knowledge and experience ◼ Management team has a track operating successful public Todd Hirsch record of successfully executing companies crucial in creating Director strategic M&A significant value for shareholders ◼ Members of the management team Former Senator Dean Heller Director sold Ascent Vision Technologies to CACI (NYSE: CACI) for ~$350 million Rear Admiral Wyman Howard in 2020 Director Source: Defense Daily, JCIC management and SEC filings. th (1) As of November 30 , 2022. 14

Why Bridger is Going Public Enhance public support and awareness of Bridger, particularly in a market without a significant number of public-ready, fundamentally-driven ESG businesses Provide public currency for strategic growth As a Public Company, Bridger Expects to Enhance its Profile and Rapidly Execute on its Strategic Attract and retain skilled employees Initiatives Ability to raise capital more efficiently Offer enhanced transparency and strong governance as the only publicly traded aerial firefighting business 15

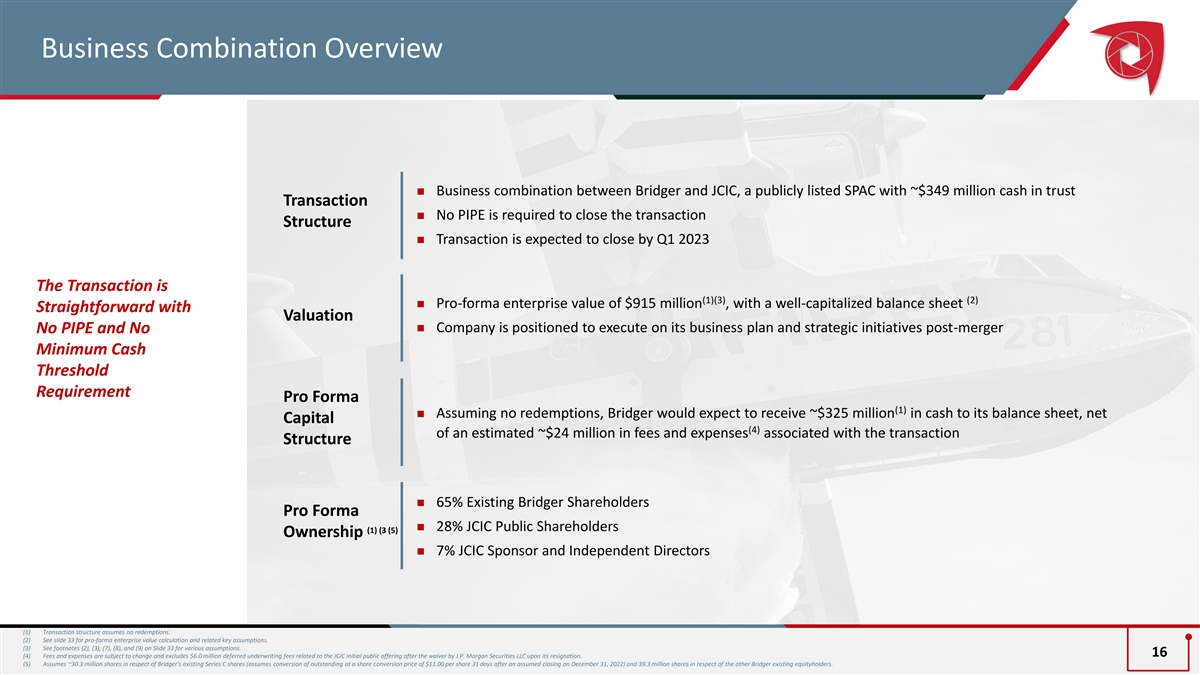

Business Combination Overview ◼ Business combination between Bridger and JCIC, a publicly listed SPAC with ~$349 million cash in trust Transaction ◼ No PIPE is required to close the transaction Structure ◼ Transaction is expected to close by Q1 2023 The Transaction is (1)(3) (2) ◼ Pro-forma enterprise value of $915 million , with a well-capitalized balance sheet Straightforward with Valuation ◼ Company is positioned to execute on its business plan and strategic initiatives post-merger No PIPE and No Minimum Cash Threshold Requirement Pro Forma (1) ◼ Assuming no redemptions, Bridger would expect to receive ~$325 million in cash to its balance sheet, net Capital (4) of an estimated ~$24 million in fees and expenses associated with the transaction Structure ◼ 65% Existing Bridger Shareholders Pro Forma ◼ 28% JCIC Public Shareholders (1) (3 (5) Ownership ◼ 7% JCIC Sponsor and Independent Directors (1) Transaction structure assumes no redemptions. (2) See slide 33 for pro-forma enterprise value calculation and related key assumptions. (3) See footnotes (2), (3), (7), (8), and (9) on Slide 33 for various assumptions. 16 (4) Fees and expenses are subject to change and excludes $6.0 million deferred underwriting fees related to the JCIC initial public offering after the waiver by J.P. Morgan Securities LLC upon its resignation. (5) Assumes ~30.3 million shares in respect of Bridger's existing Series C shares (assumes conversion of outstanding at a share conversion price of $11.00 per share 31 days after an assumed closing on December 31, 2022) and 39.3 million shares in respect of the other Bridger existing equityholders.

Investment Highlights Full Service, COCO Wildfire Fighting Platform Utilizing Leading, Purpose-Built Technology Rapidly Expanding Market Due to Increased Wildfire Season Length, Geographic Breadth and Severity Sustainability Practices: Directly Combating Major Sources of CO Emissions 2 Recurring Revenue Model Supported by Long-Term Government Contracts Near Real-Time Insight via the FireTRAC Data Integration Platform 17

The Bridger Solution

Large Market With Strong Demand for Air-Based Suppression Technologies Aerial Suppression Spend Represented ~43% … and the Market is Anticipated to Continue to Expand (1) of the $22 Billion Firefighting Market in 2021 … as Wildfires Rage Across Europe and the US Air-Based (3) Suppression Greece Faced a Disaster Wildfires Raged Across Wildfires Ravaged Across COCO of Unprecedented Southern Italy as Its Alaska with 264 Active Federal and State Proportion Rivers Dried Up Individual Fires $5.8 bn Agencies Have $9.5 bn Become Increasingly (4) (2) $0.3 bn Ground GOCO Motivated to Outsource Aerial (2) $3.2 bn GOGO Firefighting to More Effectively Combat $3.1 bn the Increasing (5) Data Presence and Intensity of Wildfires ▪ There is a rapidly growing need globally for fire suppression ▪ These events represent Summer 2022 wildfires and emphasize the assets need for increased wildfire suppression resources globally ▪ The shift away from ground towards more air-based suppression ▪ In traditional wildfire areas, wildfire intensity and duration are has already commenced increasing, and total wildfire impact is spreading into new regions as global temperatures rise ▪ Unfulfilled requests for fixed wing aircraft for aerial firefighting grew at a compound annual growth rate of 8.1% between 2002 and 2021, resulting in 1,254 unfulfilled requests in 2021 Source: National Interagency Coordination Center, CNN, CBS, The Guardian and Bridger management estimates. (1) Bridger management defines the global firefighting market as the sum of the air-based suppression, ground, and fire data, aerial imagery-related, and emergency mobile application markets. (2) GOCO: Government Owned and Contractor Operated; GOGO: Government Owned and Government Operated. (3) Based on the global aerial firefighting market size from the June 2021 Verified Market Research report and an industry estimate of the relative proportion of COCO, GOCO, and GOGO. (4) Based on Bridger management’s estimated $4.3 billion US ground market based on budgeted wildfire expenditures for key federal and state agencies; Bridger management estimated that the US ground market represented approximately 45% of the global ground market. (5) Based on Bridger management’s estimated $0.9 billion US 19 market for the fire data and surveillance-related emergency market based on review of available peer company data; Bridger management estimated that the US fire data and surveillance-related emergency market represented approximately 31% of the global fire data, aerial imagery-related, and emergency mobile application market.

Bridger’s Platform is Designed to Solve a Growing and Evolving Problem …Yet There is Inadequate Scale, Response Bridger Aerospace Provides a Wildfire Risks are Increasing… and Coordination Full-Fledged, Modern Solution ◼ Deploy highly efficient aerial firefighting assets tailored Company A Company B Company C towards diverse perimeter and suppression Operator of 4 converted Oper ator of 7 land-based tankers Operator of 9 BAE 146 (1) applications DC-10 Air Tankers and 4 CL-415s firefighting aircraft Bridger Invests in ◼ Integrate data, analytics and reporting to optimize resource deployment Tactically-Relevant ◼ Provide a fully-integrated firefighting solution to Suppression combat the escalating risks and associated carbon Technologies to Legacy fleets that rely primarily on large tankers, emissions Wildland-Urban Interface (“WUI”) Efficiently Address tailored to perimeter applications that are not as and climate change leading to (1) well-suited to serve WUI environments as Bridger more severe wildfires and and Combat the increased economic damage Growing Threat of Economic and Environmental Damage Caused by Wildfires Disparate data sources, analytics and operators result in inefficient wildfire suppression Wildfire severity increases CO 2 emissions, perpetuating global climate change Source: US Forest Service, World Resources Institute and the US Fire Administration. Note: Competitor information sourced from publicly available materials. 20 (1) See slides 22 and 23 for additional information.

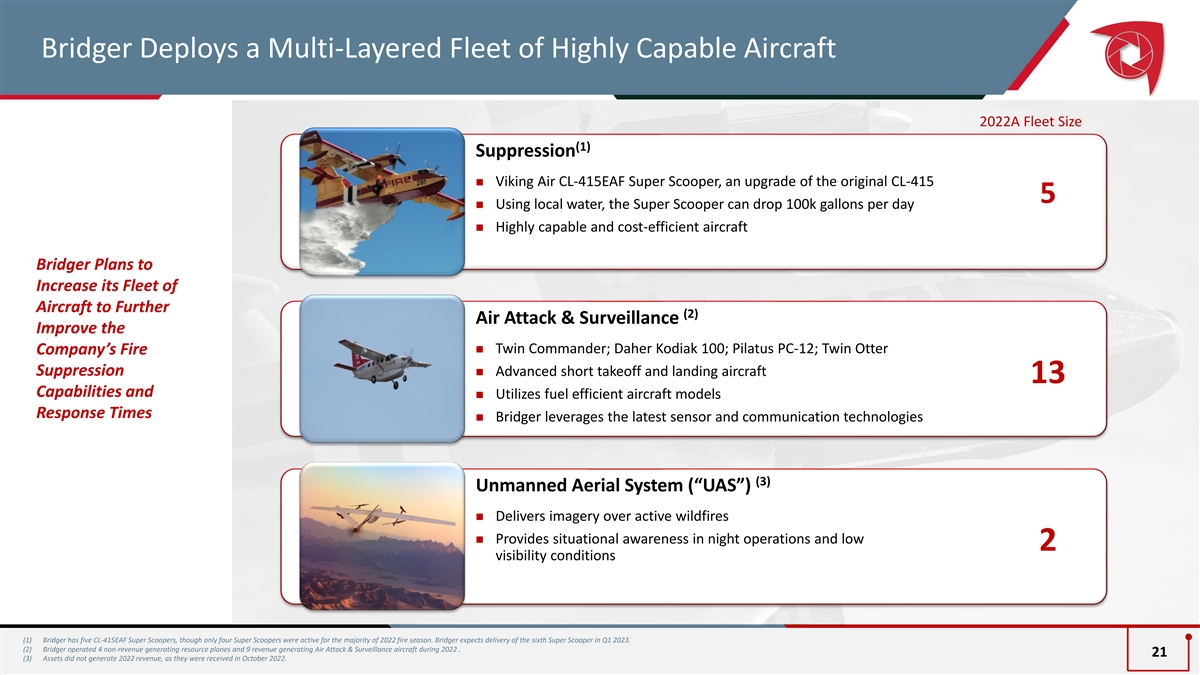

Bridger Deploys a Multi-Layered Fleet of Highly Capable Aircraft 2022A Fleet Size (1) Suppression ◼ Viking Air CL-415EAF Super Scooper, an upgrade of the original CL-415 5 ◼ Using local water, the Super Scooper can drop 100k gallons per day ◼ Highly capable and cost-efficient aircraft Bridger Plans to Increase its Fleet of Aircraft to Further (2) Air Attack & Surveillance Improve the ◼ Twin Commander; Daher Kodiak 100; Pilatus PC-12; Twin Otter Company’s Fire Suppression ◼ Advanced short takeoff and landing aircraft 13 Capabilities and ◼ Utilizes fuel efficient aircraft models Response Times ◼ Bridger leverages the latest sensor and communication technologies (3) Unmanned Aerial System (“UAS”) ◼ Delivers imagery over active wildfires ◼ Provides situational awareness in night operations and low 2 visibility conditions (1) Bridger has five CL-415EAF Super Scoopers, though only four Super Scoopers were active for the majority of 2022 fire season. Bridger expects delivery of the sixth Super Scooper in Q1 2023. (2) Bridger operated 4 non-revenue generating resource planes and 9 revenue generating Air Attack & Surveillance aircraft during 2022 . 21 (3) Assets did not generate 2022 revenue, as they were received in October 2022.

Bridger’s Scooper Fleet Provides Unique Firefighting Capabilities ◼ The CL-415EAF is an amphibious aerial firefighting aircraft outfitted with upgraded avionics and high-powered turbine engines ◼ Unique aeronautical design enables tight maneuvering at low altitudes and airspeeds, allowing for high-precision suppression ◼ Ability to utilize natural water sources enables ~50% more time-on-duty per mission than other aerial firefighting aircraft Bridger is a Scaled Owner / Operator of the CL-415EAF, a Purpose-Built Fire Suppression Aircraft 207 MPH 50% + Cruise Lower Drop Speed (1) Height 1.5k Gallons Tank 100k Capacity Gallons (2) Dropped / Day 90% of Fires Within 20 Miles of 8 Hours Scooper-accessible Daily Active (3) Bodies of Water Firefighting Time Source: National Interagency Fire Center, CalFire, WinAir, RAND Corporation, Bridger management estimates and Viking Air OEM specifications and marketing. (1) Compared to larger aerial firefighting platforms, i.e., Boeing 747 Supertanker and McDonnell Douglas DC-10. 22 (2) Assumes scoopable water is 5 miles away; a Scooper can fly up to 8 hours per day (refueling after four hours) and drop 50,000 gallons per tank of fuel. (3) Includes seasonal water bodies without regard to season and no adjustments to the suitability of a water source based on its likely size at a given time of year. Also assumes that the Company has permission to draw from these bodies of water.

Bridger Delivers More Complete and Effective Fire Suppression Capabilities Illustrative Perimeter (1) Solution Provider Multiple Layers of Aircraft Traditional LAT/VLATs Fleet Type Bridger Offers 35 Fleet Size 20 and Scaling Differentiated 100 Solutions to Combat 150-250 Drop Altitude (Feet) the Evolving (2) (feet) ~100,000 30-50,000 Daily Productivity Challenges of Aerial (Gallons) Firefighting 30 minutes - 1 hour Reload (gallo Time ns) < 1 minute Limited Near Real-time Data FireTrac Data Platform (3) (4) Direct Attack Indirect Attack Use Case “Scoopers are considerably less expensive to own and operate than larger helicopters and fixed-wing airtankers. When fires are near water, scoopers can drop more water than airtankers can drop retardant. At least two-thirds of historical fires have been within ten miles of a scooper-accessible body of water.” Rand Corporation, Air Attack Against Wildfires Source: Bridger management, Viking Air OEM specifications and marketing. (1) Based on comparisons to large air tankers (“LAT”) and very large air tankers (“VLAT”) that primarily drop retardants. (2) Assumes scoopable water is 5 miles away; a Scooper can fly up to 8 hours per day (refueling after four hours) and drop 50,000 gallons per tank of fuel. 23 (3) Indirect Attack platforms are retardant-based and are used to create a fire line, preventing further spread of flames. (4) Direct Attack platforms are water-based and are dropped directly on flames to combat wildfires immediately.

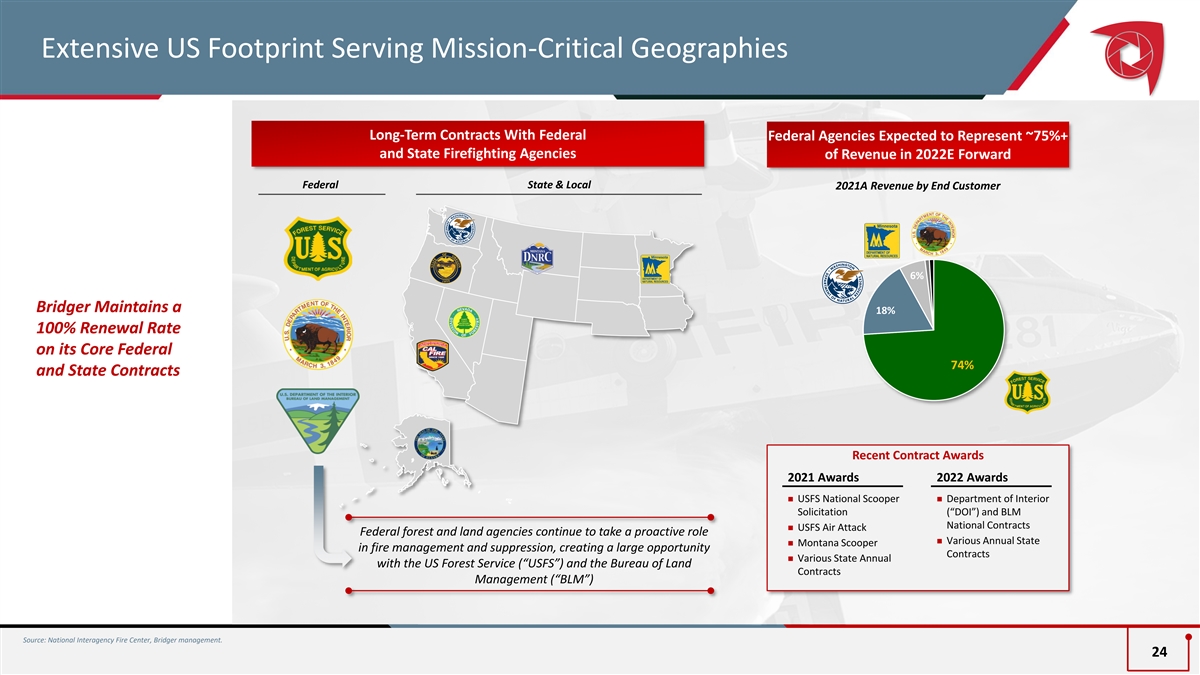

Extensive US Footprint Serving Mission-Critical Geographies Long-Term Contracts With Federal Federal Agencies Expected to Represent ~75%+ and State Firefighting Agencies of Revenue in 2022E Forward Federal State & Local 2021A Revenue by End Customer 6% Bridger Maintains a 18% 100% Renewal Rate on its Core Federal 74% and State Contracts Recent Contract Awards 2021 Awards 2022 Awards ◼ USFS National Scooper ◼ Department of Interior Solicitation (“DOI”) and BLM National Contracts ◼ USFS Air Attack Federal forest and land agencies continue to take a proactive role ◼ Various Annual State ◼ Montana Scooper in fire management and suppression, creating a large opportunity Contracts ◼ Various State Annual with the US Forest Service (“USFS”) and the Bureau of Land Contracts Management (“BLM”) Source: National Interagency Fire Center, Bridger management. 24

FireTrac: Next-Gen Wildfire Data, Surveillance and Reporting Platform Data Technology ◼ Combine Bridger’s proprietary in-flight imaging capabilities with ◼ Near real-time interface to inform users of potential wildfire impacts published governmental data ◼ Interactive mapping solutions to help visualize fires within a ◼ Consolidated information, imagery and data regarding critical wildfire geospatial context incidents ◼ Provide push notifications of detected activity near watched (1) ◼ Layered data to analyze fire intensity, size, addresses to a user’s mobile device location and weather patterns FireTrac Integrates ◼ Centralized information source for near real-time, relevant wildfire data Proprietary Data and Technology to Deliver Leading fire map and sensor data capabilities Unique Insights on ✓ Fire Risk Near real-time imagery of key fire incidents ✓ Satellite and weather data ✓ User uploaded data ✓ Social media style Hive-based reporting and updates ✓ Source: National Interagency Fire Center, Bridger management. (1) Future release feature. 25

Financial Overview

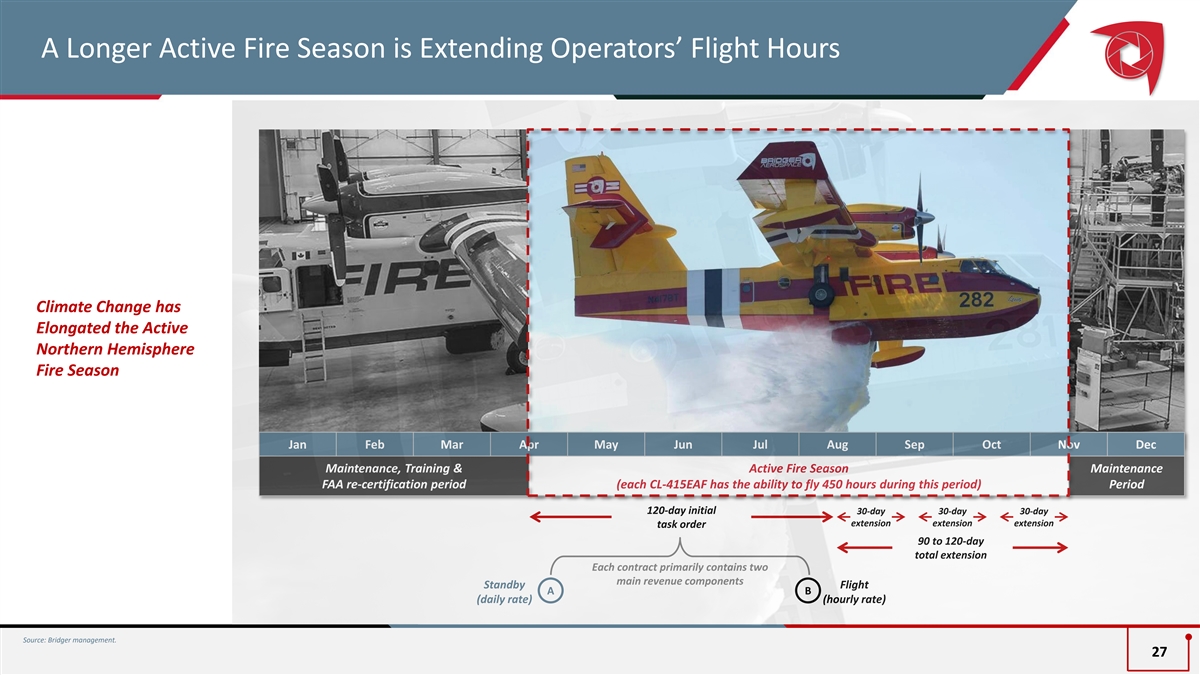

A Longer Active Fire Season is Extending Operators’ Flight Hours Climate Change has Elongated the Active Northern Hemisphere Fire Season Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Maintenance, Training & Active Fire Season Maintenance FAA re-certification period (each CL-415EAF has the ability to fly 450 hours during this period) Period 120-day initial 30-day 30-day 30-day extension extension extension task order 90 to 120-day total extension Each contract primarily contains two main revenue components Standby Flight A B (daily rate) (hourly rate) Source: Bridger management. 27

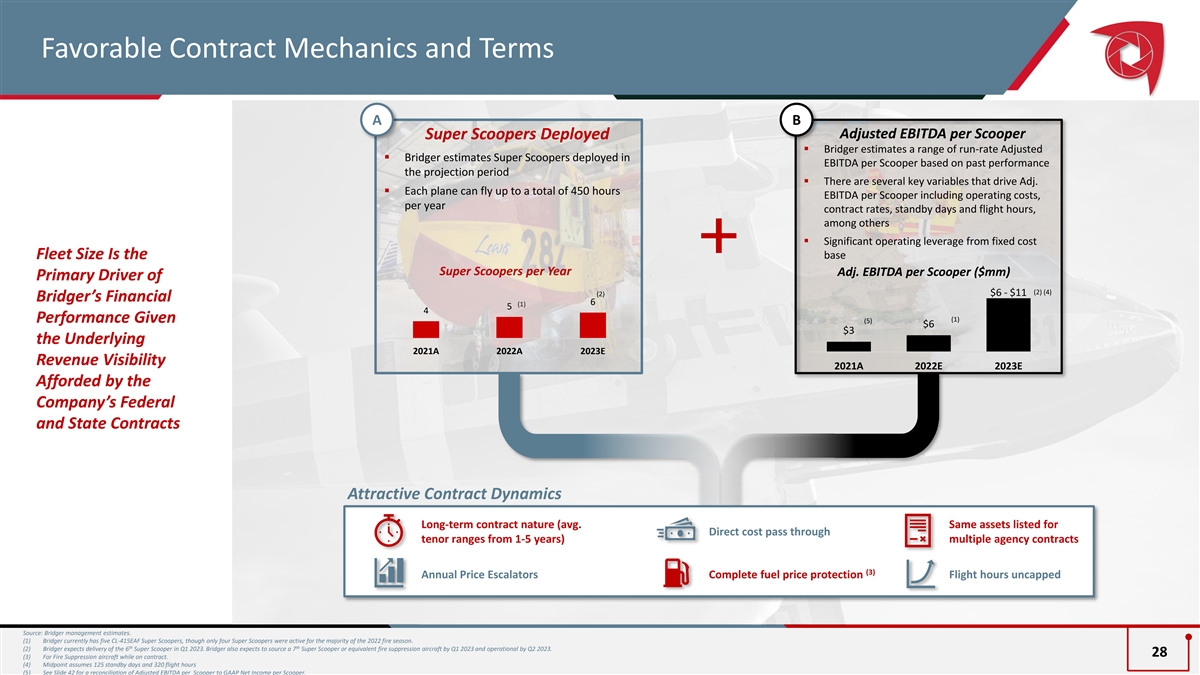

Favorable Contract Mechanics and Terms A B Super Scoopers Deployed Adjusted EBITDA per Scooper ▪ Bridger estimates a range of run-rate Adjusted ▪ Bridger estimates Super Scoopers deployed in EBITDA per Scooper based on past performance the projection period ▪ There are several key variables that drive Adj. ▪ Each plane can fly up to a total of 450 hours EBITDA per Scooper including operating costs, per year contract rates, standby days and flight hours, among others ▪ Significant operating leverage from fixed cost Fleet Size Is the base Super Scoopers per Year Adj. EBITDA per Scooper ($mm) Primary Driver of (2) (4) $6 - $11 (2) Bridger’s Financial 6 (1) 5 4 (1) Performance Given (5) $6 $3 the Underlying 2021A 2022A 2023E Revenue Visibility 2021A 2022E 2023E Afforded by the Company’s Federal and State Contracts Attractive Contract Dynamics Long-term contract nature (avg. Same assets listed for Direct cost pass through tenor ranges from 1-5 years) multiple agency contracts (3) Annual Price Escalators Complete fuel price protection Flight hours uncapped Source: Bridger management estimates. (1) Bridger currently has five CL-415EAF Super Scoopers, though only four Super Scoopers were active for the majority of the 2022 fire season. th th (2) Bridger expects delivery of the 6 Super Scooper in Q1 2023. Bridger also expects to source a 7 Super Scooper or equivalent fire suppression aircraft by Q1 2023 and operational by Q2 2023. 28 (3) For Fire Suppression aircraft while on contract. (4) Midpoint assumes 125 standby days and 320 flight hours (5) See Slide 42 for a reconciliation of Adjusted EBITDA per Scooper to GAAP Net Income per Scooper.

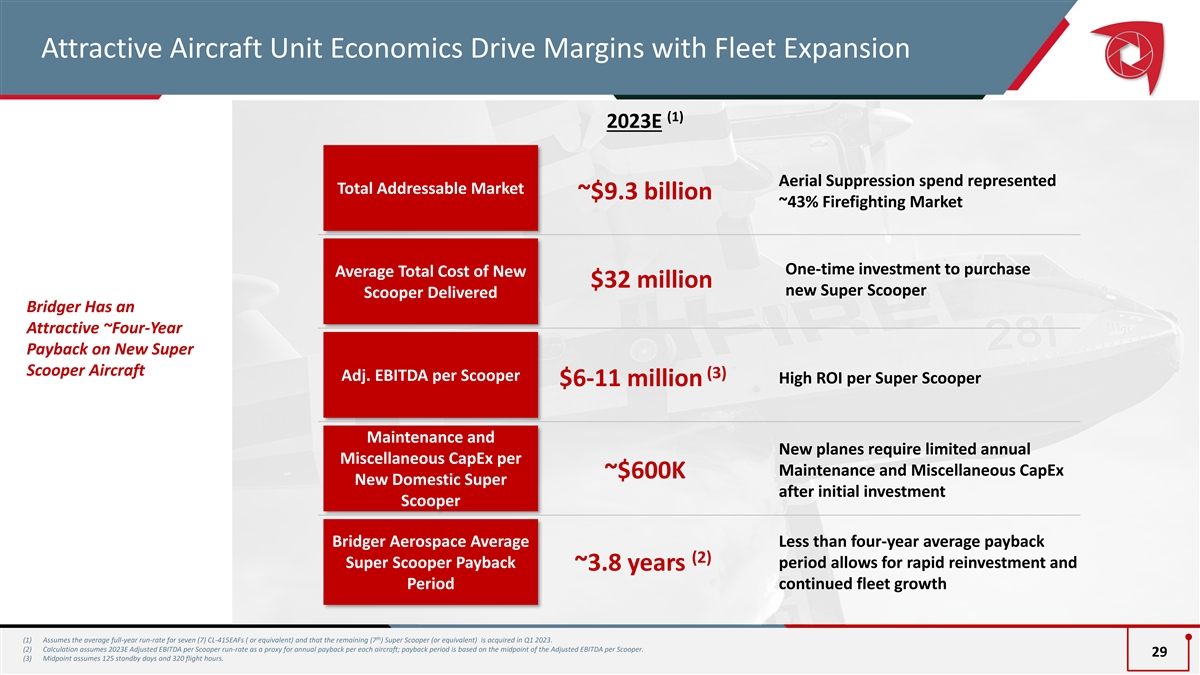

Attractive Aircraft Unit Economics Drive Margins with Fleet Expansion (1) 2023E Aerial Suppression spend represented Total Addressable Market ~$9.3 billion ~43% Firefighting Market One-time investment to purchase Average Total Cost of New $32 million new Super Scooper Scooper Delivered Bridger Has an Attractive ~Four-Year Payback on New Super Scooper Aircraft (3) Adj. EBITDA per Scooper High ROI per Super Scooper $6-11 million Maintenance and New planes require limited annual Miscellaneous CapEx per Maintenance and Miscellaneous CapEx ~$600K New Domestic Super after initial investment Scooper Bridger Aerospace Average Less than four-year average payback (2) Super Scooper Payback period allows for rapid reinvestment and ~3.8 years Period continued fleet growth th (1) Assumes the average full-year run-rate for seven (7) CL-415EAFs ( or equivalent) and that the remaining (7 ) Super Scooper (or equivalent) is acquired in Q1 2023. (2) Calculation assumes 2023E Adjusted EBITDA per Scooper run-rate as a proxy for annual payback per each aircraft; payback period is based on the midpoint of the Adjusted EBITDA per Scooper. 29 (3) Midpoint assumes 125 standby days and 320 flight hours.

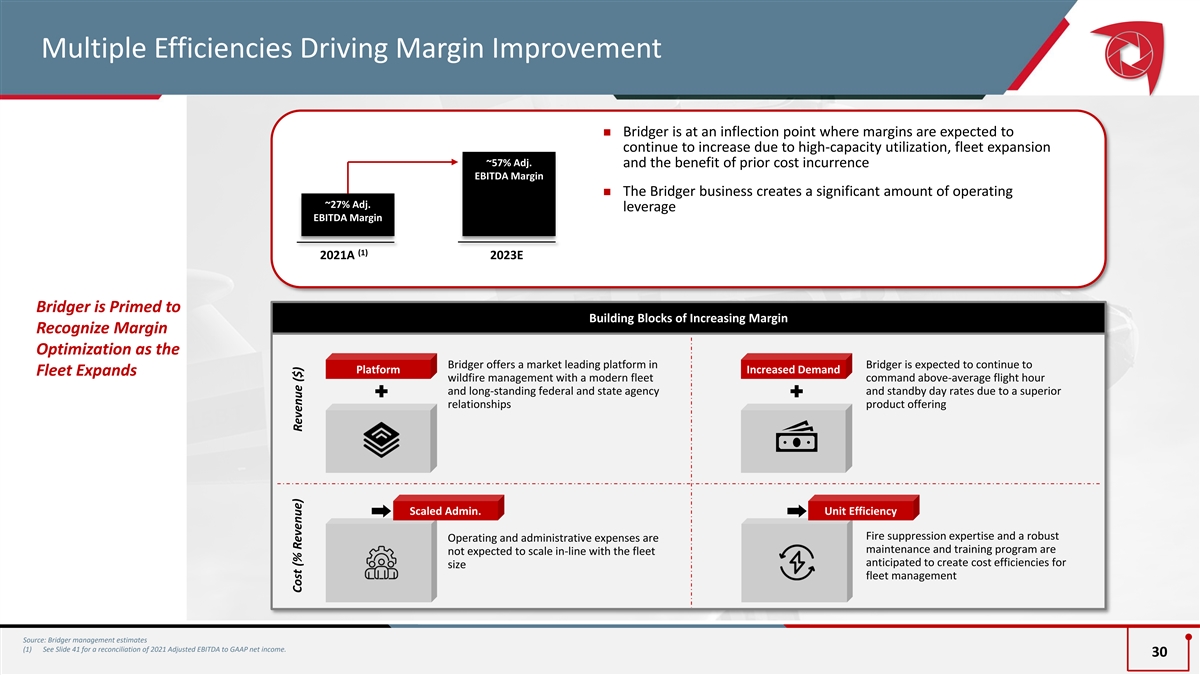

Multiple Efficiencies Driving Margin Improvement ◼ Bridger is at an inflection point where margins are expected to continue to increase due to high-capacity utilization, fleet expansion ~57% Adj. and the benefit of prior cost incurrence EBITDA Margin ◼ The Bridger business creates a significant amount of operating ~27% Adj. leverage EBITDA Margin (1) 2021A 2023E Bridger is Primed to Building Blocks of Increasing Margin Recognize Margin Optimization as the Bridger offers a market leading platform in Bridger is expected to continue to Platform Increased Demand Fleet Expands wildfire management with a modern fleet command above-average flight hour and long-standing federal and state agency and standby day rates due to a superior relationships product offering Scaled Admin. Unit Efficiency Fire suppression expertise and a robust Operating and administrative expenses are maintenance and training program are not expected to scale in-line with the fleet anticipated to create cost efficiencies for size fleet management Source: Bridger management estimates (1) See Slide 41 for a reconciliation of 2021 Adjusted EBITDA to GAAP net income. 30 Cost (% Revenue) Revenue ($)

Financial Overview ) ($ In Millions 2021A 2022E 2023E Pro Forma Valuation ◼ Although Bridger’s Super Scooper fleet only comprises ~30% Fire Suppression $30 $39 $85 of total fleet count, the CL-415EAF’s leading operating Air Attack 8 7 13 performance contributes to the majority of top-line sales via UAS 1 0 3 higher contracted rates Other (Maintenance, Admin) 0 0 1 ◼ Bridger’s growth capital expenditures are focused on Total Revenue $39 $46 $102 expanding the CL-415EAF / fire suppression fleet (7) Less: COGS (26) (34) (35) ◼ Bridger operated nearly the entire 2022 fire season with 4 Gross Profit $13 $12 $67 Super Scoopers. Bridger expects to have 6 Scoopers and 1 Gross Profit Margin % 33% 26% 66% Scooper equivalent in possession ahead of the 2023 fire (8) season Less: G&A, Interest Expense, and Other Income (19) (55) (29) (6) Net Income (Loss) $(7) $(43) $38 ◼ Expenses associated with operating additional CL-415EAF aircraft are not expected to scale in-line with revenue (1) (5) Adj. EBITDA $11 $4 $58 growth Adj. EBITDA Margin % 27% 10% 57% − Bridger gains incremental operating leverage as more Maintenance and Miscellaneous CapEx (6) (14) (6) Super Scoopers are acquired (2) Free Cash Flow $5 $(10) $51 ◼ Cash on hand from the Series C capital raise, municipal bond Growth CapEx $54 $34 $79 financing and free cash flow generation is projected to fully finance Bridger’s growth projections (3) (4) # of Fire Suppression Aircraft 4 5 7 (4) # of Air Attack & Surveillance Aircraft 12 13 18 Source: Bridger management estimates. (1) See slide 41 for a reconciliation of GAAP Net Income to 2021A EBITDA. (2) Defined as Adj. EBITDA less Maintenance and Miscellaneous CapEx. (3) Bridger has five CL-415EAF Super Scoopers, though only four Super Scoopers were active for the majority of 2022 fire season. (4) Bridger expects delivery of the sixth Super Scooper in Q1 2023. Assumes acquisition of additional aircrafts, including possibility of purchasing fewer but larger Air Attack planes with equivalent revenue impact, resulting in a smaller fleet size. Assumes conversion of two resource planes to Air Attack. (5) Adjusted EBITDA for 2022E includes (among other items) (i) lower revenue than anticipated due to the 31 delayed arrival of multipleaircraft and the impact of a less intense fire season as compared to the prior two years, (ii) $3.0 million of costs related tothe acquisition of Super Scoopers 5 and 6, (ii) $2.2 million of business development related expenses and (iii) $0.4 for the development of FireTrac. (6) May not foot due to rounding. (7) Includes depreciation of $5M, $9M, and $8M in COGS for 2021A, 2022E and 2023E, respectively. (8) Includes depreciation and interest expense.

Transaction Details and Benchmarking

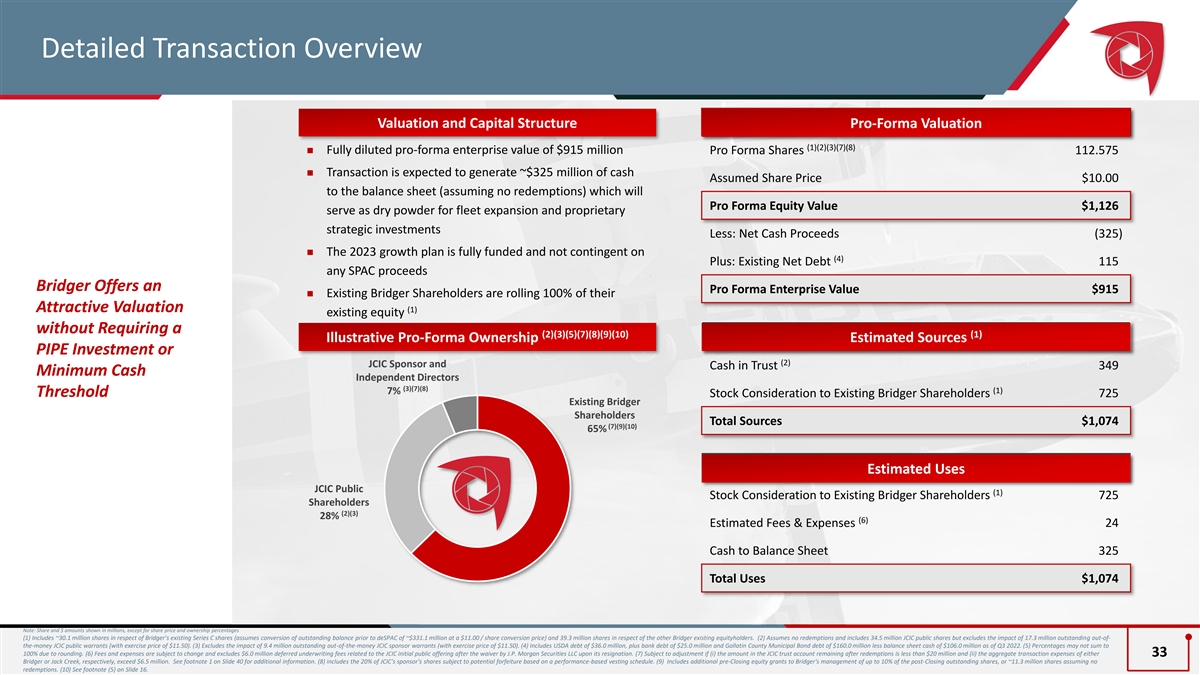

Detailed Transaction Overview Pro Forma Valuation Valuation and Capital Structure Pro-Forma Valuation (1)(2)(3)(7)(8) ◼ Fully diluted pro-forma enterprise value of $915 million Pro Forma Shares 112.575 ◼ Transaction is expected to generate ~$325 million of cash Assumed Share Price $10.00 to the balance sheet (assuming no redemptions) which will Pro Forma Equity Value $1,126 serve as dry powder for fleet expansion and proprietary strategic investments Less: Net Cash Proceeds (325) ◼ The 2023 growth plan is fully funded and not contingent on (4) Plus: Existing Net Debt 115 any SPAC proceeds Bridger Offers an Pro Forma Enterprise Value $915 ◼ Existing Bridger Shareholders are rolling 100% of their Attractive Valuation (1) existing equity without Requiring a (2)(3)(5)(7)(8)(9)(10) (1) Illustrative Pro-Forma Ownership EstimaSour ted Sour ces ces PIPE Investment or (2) JCIC Sponsor and Cash in Trust 349 Minimum Cash Independent Directors (3)(7)(8) (1) 7% Threshold Stock Consideration to Existing Bridger Shareholders 725 Existing Bridger Shareholders Total Sources $1,074 (7)(9)(10) 65% Uses Estimated Uses JCIC Public (1) Stock Consideration to Existing Bridger Shareholders 725 Shareholders (2)(3) 28% (6) Estimated Fees & Expenses 24 Cash to Balance Sheet 325 Total Uses $1,074 Note: Share and $ amounts shown in millions, except for share price and ownership percentages (1) Includes ~30.1 million shares in respect of Bridger’s existing Series C shares (assumes conversion of outstanding balance prior to deSPAC of ~$331.1 million at a $11.00 / share conversion price) and 39.3 million shares in respect of the other Bridger existing equityholders. (2) Assumes no redemptions and includes 34.5 million JCIC public shares but excludes the impact of 17.3 million outstanding out-of- the-money JCIC public warrants (with exercise price of $11.50). (3) Excludes the impact of 9.4 million outstanding out-of-the-money JCIC sponsor warrants (with exercise price of $11.50). (4) Includes USDA debt of $36.0 million, plus bank debt of $25.0 million and Gallatin County Municipal Bond debt of $160.0 million less balance sheet cash of $106.0 million as of Q3 2022. (5) Percentages may not sum to 100% due to rounding. (6) Fees and expenses are subject to change and excludes $6.0 million deferred underwriting fees related to the JCIC initial public offering after the waiver by J.P. Morgan Securities LLC upon its resignation. (7) Subject to adjustment if (i) the amount in the JCIC trust account remaining after redemptions is less than $20 million and (ii) the aggregate transaction expenses of either 33 Bridger or Jack Creek, respectively, exceed $6.5 million. See footnote 1 on Slide 40 for additional information. (8) includes the 20% of JCIC's sponsor's shares subject to potential forfeiture based on a performance-based vesting schedule. (9) Includes additional pre-Closing equity grants to Bridger's management of up to 10% of the post-Closing outstanding shares, or ~11.3 million shares assuming no redemptions. (10) See footnote (5) on Slide 16.

Operational Benchmarking CY2023E Revenue Growth 122% C CY202 Y2023 3E E Defens Defens e eElectroni Electron cs ics Median = 8% Median = 22% 60% C CY202 Y2023 3E ES S pec peialty cialt y A vi Avi ation ation Median = Median = 11% 27% 14% 49% 12% 11% 10% 11% 10% 28% 27% 25% 25% 22% 18% 21% 6% 4% 4% 11% Bridger’s Projected Revenue Growth and Margin Profile are Favorable Versus Peers CY2023E Adj. EBITDA Margin CY2023E Defense Electronics Median = 22% CY2023E Defense Electronics Median = 21% 60% C CY202 Y2023 3E ES S pec peialty cialt y A vi Avi ation ation Median = Median = 27% 27% 50% 57% 49% 28% 27% 25% 27% 27% 25% 22% 18% 24% 21% 24% 21% 21% 18% 11% 9% Source: CapIQ, Company Management, BAMSEC, public filings as of November 30, 2022. 34

Appendix

Rising and Evolving Wildfire Risks Threaten Communities More Severe Wildfire Season Wildland-Urban Interface Changes in Temperatures and Insufficient Firefighting Capacity Lack of Real-Time Insights Precipitation Levels Are Increasing the Magnitude of Wildfires and Adding Weeks to Destructive Fire Seasons “The challenge is huge. We now have around 70,000 communities at risk from wildfire, and only 6,000 of them — less than 10 percent — have community wildfire protection plans.” Tom Tidwell - Former Chief of the United States Forest Service Source: US Forest Service, Bridger management. 36

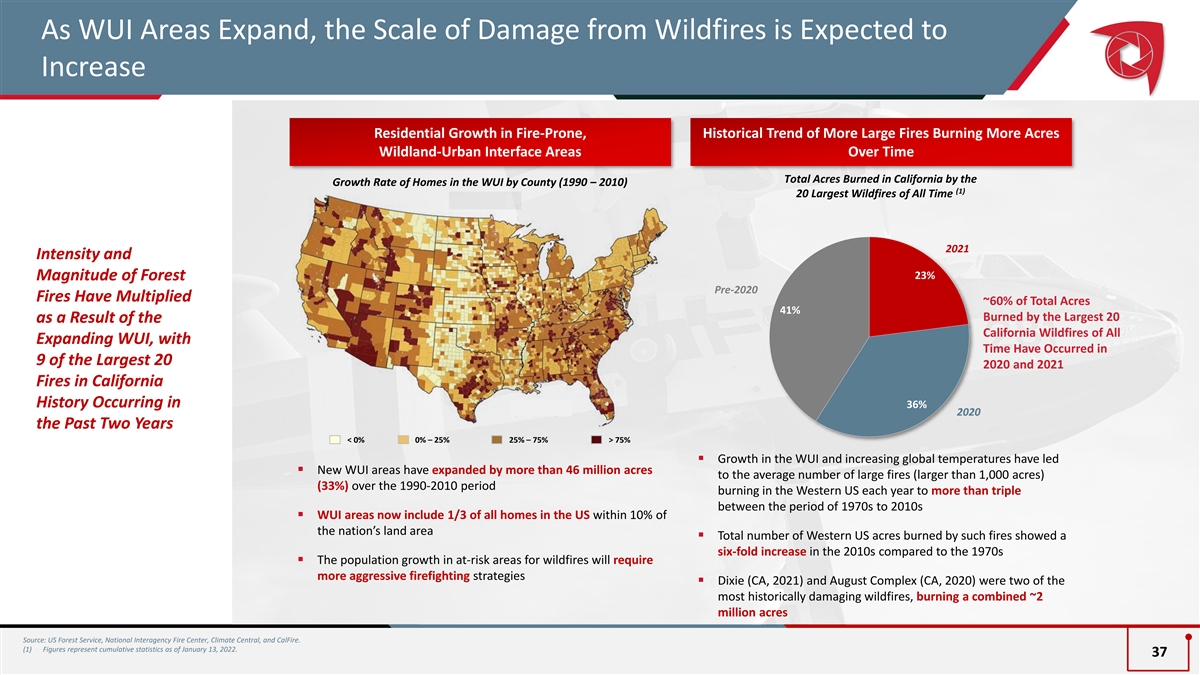

As WUI Areas Expand, the Scale of Damage from Wildfires is Expected to Increase Residential Growth in Fire-Prone, Historical Trend of More Large Fires Burning More Acres Wildland-Urban Interface Areas Over Time Total Acres Burned in California by the Growth Rate of Homes in the WUI by County (1990 – 2010) (1) 20 Largest Wildfires of All Time 2021 Intensity and 23% Magnitude of Forest Pre-2020 Fires Have Multiplied ~60% of Total Acres 41% Burned by the Largest 20 as a Result of the California Wildfires of All Expanding WUI, with Time Have Occurred in 9 of the Largest 20 2020 and 2021 Fires in California History Occurring in 36% 2020 2020 the Past Two Years < 0% 0% – 25% 25% – 75% > 75% ▪ Growth in the WUI and increasing global temperatures have led ▪ New WUI areas have expanded by more than 46 million acres to the average number of large fires (larger than 1,000 acres) (33%) over the 1990-2010 period burning in the Western US each year to more than triple between the period of 1970s to 2010s ▪ WUI areas now include 1/3 of all homes in the US within 10% of the nation’s land area ▪ Total number of Western US acres burned by such fires showed a six-fold increase in the 2010s compared to the 1970s ▪ The population growth in at-risk areas for wildfires will require more aggressive firefighting strategies ▪ Dixie (CA, 2021) and August Complex (CA, 2020) were two of the most historically damaging wildfires, burning a combined ~2 million acres Source: US Forest Service, National Interagency Fire Center, Climate Central, and CalFire. (1) Figures represent cumulative statistics as of January 13, 2022. 37

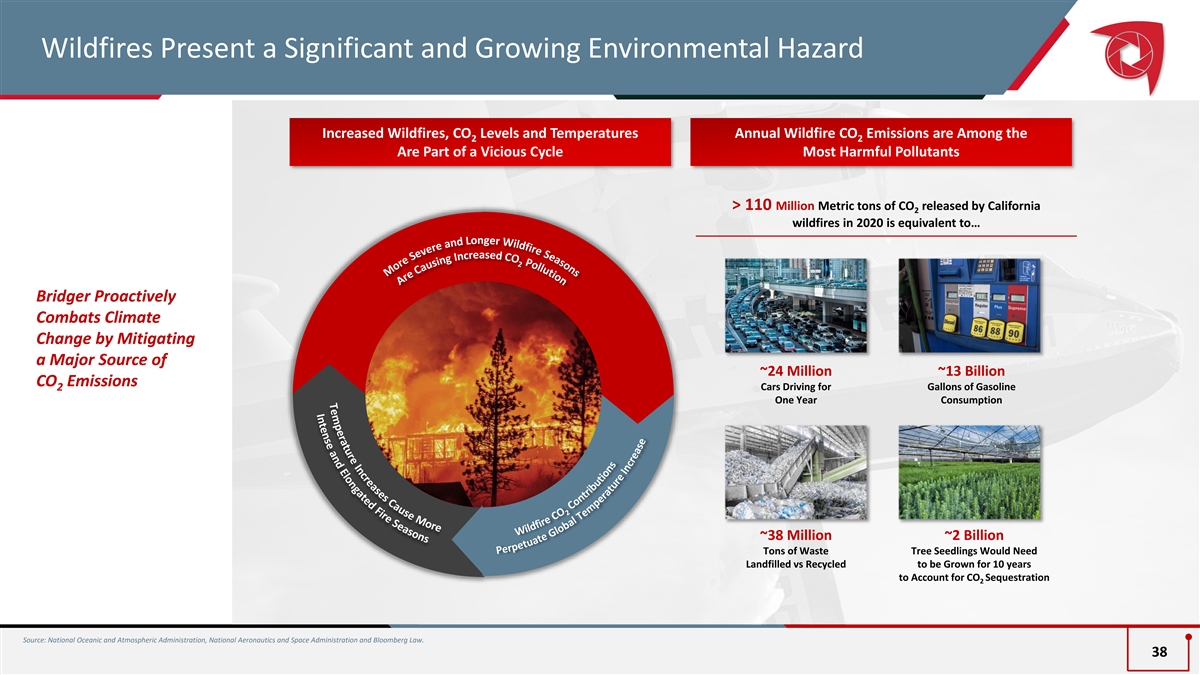

Wildfires Present a Significant and Growing Environmental Hazard Increased Wildfires, CO Levels and Temperatures Annual Wildfire CO Emissions are Among the 2 2 Are Part of a Vicious Cycle Most Harmful Pollutants > 110 Million Metric tons of CO released by California 2 wildfires in 2020 is equivalent to… Bridger Proactively Combats Climate Change by Mitigating a Major Source of ~24 Million ~13 Billion CO Emissions 2 Cars Driving for Gallons of Gasoline One Year Consumption ~38 Million ~2 Billion Tons of Waste Tree Seedlings Would Need Landfilled vs Recycled to be Grown for 10 years to Account for CO Sequestration 2 Source: National Oceanic and Atmospheric Administration, National Aeronautics and Space Administration and Bloomberg Law. 38

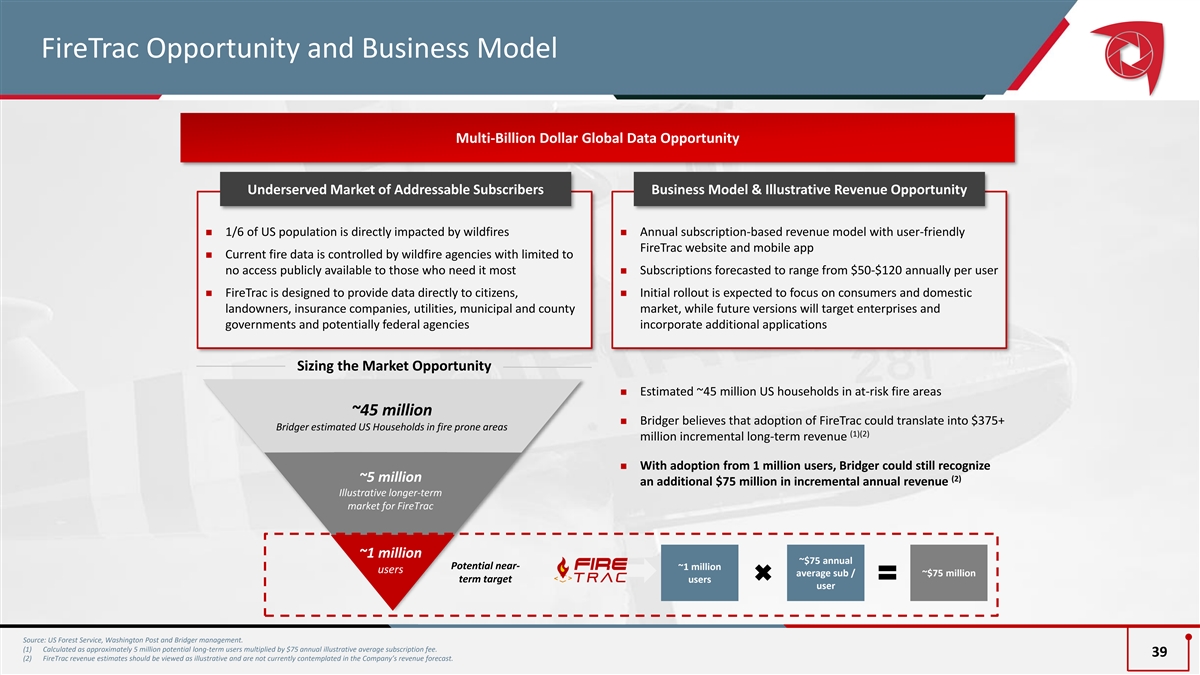

FireTrac Opportunity and Business Model Multi-Billion Dollar Global Data Opportunity Underserved Market of Addressable Subscribers Business Model & Illustrative Revenue Opportunity ◼ 1/6 of US population is directly impacted by wildfires◼ Annual subscription-based revenue model with user-friendly FireTrac website and mobile app ◼ Current fire data is controlled by wildfire agencies with limited to no access publicly available to those who need it most◼ Subscriptions forecasted to range from $50-$120 annually per user ◼ FireTrac is designed to provide data directly to citizens, ◼ Initial rollout is expected to focus on consumers and domestic landowners, insurance companies, utilities, municipal and county market, while future versions will target enterprises and governments and potentially federal agencies incorporate additional applications Sizing the Market Opportunity ◼ Estimated ~45 million US households in at-risk fire areas ~45 million ◼ Bridger believes that adoption of FireTrac could translate into $375+ Bridger estimated US Households in fire prone areas (1)(2) million incremental long-term revenue ◼ With adoption from 1 million users, Bridger could still recognize ~5 million (2) an additional $75 million in incremental annual revenue Illustrative longer-term market for FireTrac ~1 million ~$75 annual Potential near- ~1 million users average sub / ~$75 million term target users user Source: US Forest Service, Washington Post and Bridger management. (1) Calculated as approximately 5 million potential long-term users multiplied by $75 annual illustrative average subscription fee. 39 (2) FireTrac revenue estimates should be viewed as illustrative and are not currently contemplated in the Company’s revenue forecast.

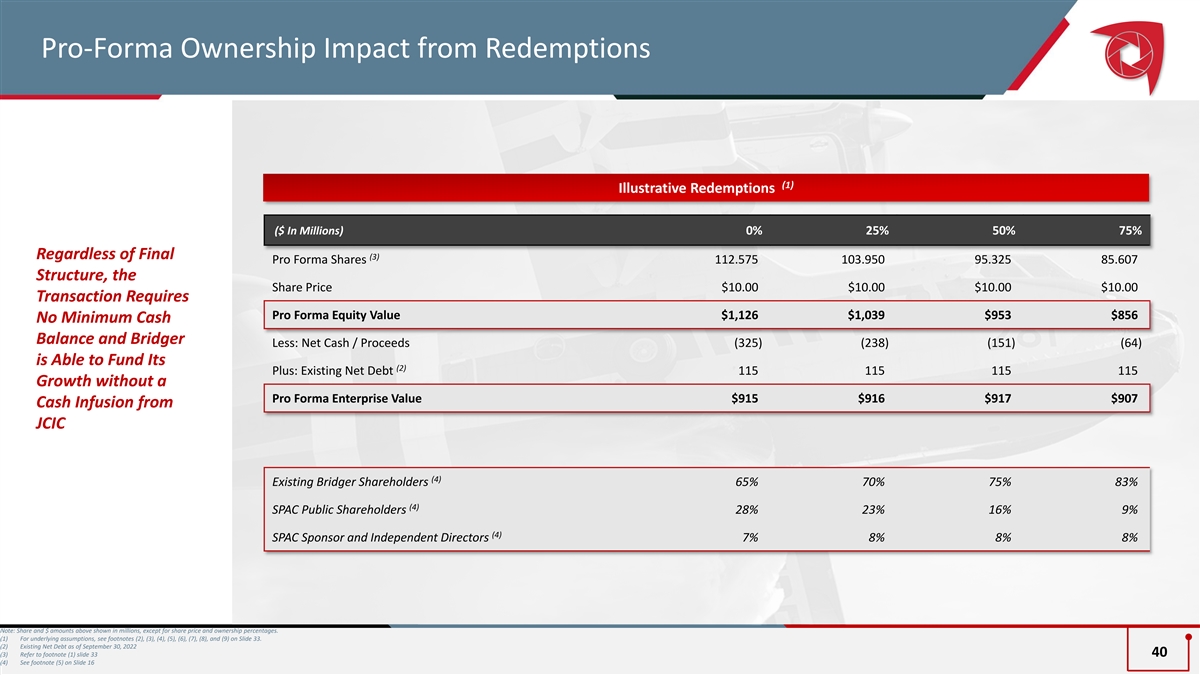

Pro-Forma Ownership Impact from Redemptions (1) Illustrative Redemptions ($ In Millions) 0% 25% 50% 75% Regardless of Final (3) Pro Forma Shares 112.575 103.950 95.325 85.607 Structure, the Share Price $10.00 $10.00 $10.00 $10.00 Transaction Requires Pro Forma Equity Value $1,126 $1,039 $953 $856 No Minimum Cash Balance and Bridger Less: Net Cash / Proceeds (325) (238) (151) (64) is Able to Fund Its (2) Plus: Existing Net Debt 115 115 115 115 Growth without a Pro Forma Enterprise Value $915 $916 $917 $907 Cash Infusion from JCIC (4) Existing Bridger Shareholders 65% 70% 75% 83% (4) SPAC Public Shareholders 28% 23% 16% 9% (4) SPAC Sponsor and Independent Directors 7% 8% 8% 8% Note: Share and $ amounts above shown in millions, except for share price and ownership percentages. (1) For underlying assumptions, see footnotes (2), (3), (4), (5), (6), (7), (8), and (9) on Slide 33. (2) Existing Net Debt as of September 30, 2022 (3) Refer to footnote (1) slide 33 40 (4) See footnote (5) on Slide 16

Net Income to Adjusted EBITDA Reconciliation 2021A Net Loss to Adjusted EBITDA Reconciliation Year Ended December 31, 2021 ($ In Millions) Net Loss ($6.5) Depreciation and Amortization 6.7 Interest Expenses 9.3 EBITDA $9.4 (1) Loss on Disposals 1.0 (2) Legal Fees 0.1 Adj. EBITDA $10.5 (3) Net Income / Net (Loss) Margin (17%) (3) Adj. EBITDA Margin % 27% Note: Figures shown above in $, except for margin percentages. (1) Represented loss on the disposal or obsolescence of aging aircraft. 41 (2) Represents one-time costs associated with legal fees for financing activities. (3) Net loss margin represents net loss divided by total revenue and Adj. EBITDA margin represents Adj. EBITDA divided by total revenue.

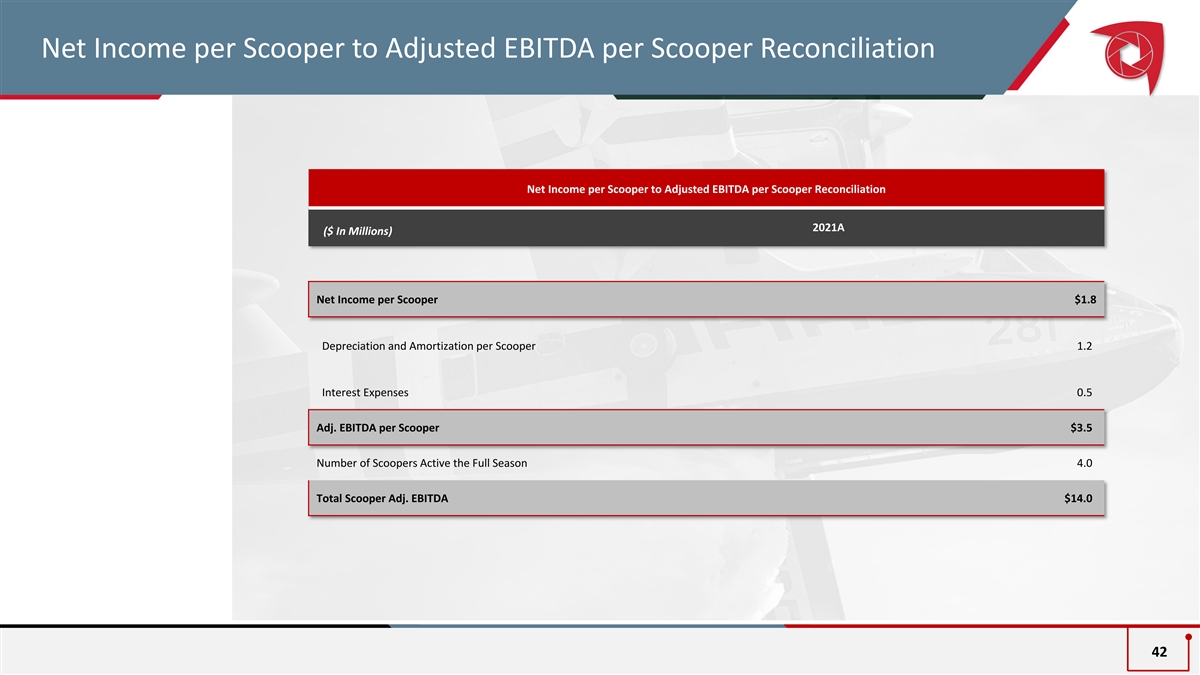

Net Income per Scooper to Adjusted EBITDA per Scooper Reconciliation Net Income per Scooper to Adjusted EBITDA per Scooper Reconciliation 2021A ($ In Millions) Net Income per Scooper $1.8 Depreciation and Amortization per Scooper 1.2 Interest Expenses 0.5 Adj. EBITDA per Scooper $3.5 Number of Scoopers Active the Full Season 4.0 Total Scooper Adj. EBITDA $14.0 42

Risk Factors (1 of 5) All references to “Bridger,” the “Company,” “we,” “us” or “our” refer to the business of Bridger Aerospace Group Holdings, LLC and its consolidated subsidiaries. The risks presented below are certain of the general risks related to our business, industry and ownership structure and are not exhaustive. Additional risks that we currently do not know about or that we currently believe to be immaterial may also impair our business, financial condition or results of operations. The list below is qualified in its entirety by disclosures contained in future filings by the Company, or by third parties (including Jack Creek Investment Corp. (“Jack Creek”)) with respect to the Company, with the United States Securities and Exchange Commission (“SEC”). These risks speak only as of the date of this presentation and the Company makes no commitment to update such disclosure. The risks highlighted in future filings with the SEC may differ significantly from, and will be more extensive than, those presented below. Aviation and Firefighting Risks ▪ Our operation of aircraft involves a degree of inherent risk, and we could suffer losses and adverse publicity stemming from any accident, whether related to us or not, involving aircraft, helicopters, or commercial drones similar to the assets we use in our operations. ▪ Our business is inherently risky in that it is fighting wildfires which are powerful and unpredictable. ▪ The unavailability of an aircraft due to loss, delayed delivery of new aircraft, mechanical failure, lack of pilots or mechanical personnel, especially one of the Viking Air CL-415EAFs (a Super Scooper), would result in lower operating revenues for us for a period of time that cannot be determined and would likely be prolonged. ▪ Our pilots and mechanics are required by contract to meet a minimum standard of operational experience. Finding and employing individuals with the necessary level of experience and certification has required us to hire U.S. and Canadian personnel. Inability to source and hire personnel with appropriate skills and experience would inhibit operations. ▪ The development of superior alternative firefighting tactics or technology that do not rely on our existing and planned capital assets could reduce demand for our services and result in a material reduction in our revenue and results of operations. Operations Risks ▪ We rely on our information technology systems to manage numerous aspects of our business. A cyber-based attack of these systems could disrupt our ability to deliver services to our customers and could lead to increased overhead costs, decreased sales, and harm to our reputation. ▪ Our service, data and systems may be critical to operations or involve the storage, processing and transmission of sensitive data, including valuable intellectual property, other proprietary or confidential data, regulated data, and personal information of employees, and others. Successful breaches, employee malfeasance, or human or technological error could result in, for example, unauthorized access to, disclosure, modification, misuse, loss, or destruction of our or other third-party data or systems; theft of sensitive, regulated, or confidential data including personal information and intellectual property; the loss of access to critical data or systems; service or system disruptions or denials of service. ▪ Failure to comply with federal, state and foreign laws and regulations relating to privacy, data protection and consumer protection, or the expansion of current laws and regulations or the enactment of new laws or regulations in these areas, could adversely affect our business and our financial condition. ▪ Our reputation and ability to do business may be impacted by the improper conduct of our employees, agents or business partners. ▪ Any failure to offer high-quality aerial firefighting services to customers may harm our relationships with our customers and could adversely affect our reputation, brand, business, financial condition, and results of operations. ▪ Natural disasters, unusual weather conditions, pandemic or epidemic outbreaks, terrorist acts and political events could disrupt our business. ▪ We are subject to risks associated with climate change, including the potential increased impacts of severe weather events on our operations and infrastructure, and changes in weather patterns may result in lower demand for our services if such changes result in a reduced risk of wildfires. ▪ Our business is dependent on the availability of aircraft fuel. Continued periods of significant disruption in the supply or cost of aircraft fuel could have a significant negative impact on consumer demand, our operating results, and liquidity. 43

Risk Factors (2 of 5) Operations Risks (continued) ▪ System failures, defects, errors, or vulnerabilities in our website, applications, backend systems, or other technology systems or those of third-party technology providers could harm our reputation and brand and adversely impact our business, financial condition, and results of operations. ▪ If we fail to adequately protect our proprietary intellectual property rights, our competitive position could be impaired and we may lose market share, generate reduced revenue, and/or incur costly litigation to protect our rights. ▪ We use open-source software in connection with our platform, which may pose risks to our intellectual property. ▪ Our insurance may become too difficult or expensive for us to obtain or maintain. Increases in insurance costs or reductions in insurance coverage may materially and adversely impact our results of operations and financial position. ▪ We are highly dependent on our senior management team and other highly skilled personnel with unique skills. We will need to be able to continue to grow our workforce with highly skilled workers in the future. If we are not successful in attracting or retaining highly qualified personnel, we may not be able to successfully implement our business strategy. ▪ Our business may be adversely affected by labor and union activities. ▪ Past performance by our management team or their respective affiliates may not be indicative of future performance of an investment in us. ▪ We have entered into ground leases with terms of twenty (20) and ten (10) years with the Gallatin Airport Authority for each of our hangars. If the Airport Authority declines to renew any of our ground leases, our operations and results of operations could be materially and adversely impacted. ▪ Our lack of diversification with respect to the aircrafts we use may subject us to negative economic, competitive and regulatory developments that disproportionately impact our aviation assets as compared to other fire suppression aircraft or alternative fire suppression services, which could adversely affect our ability to market and sell our services and our reputation. ▪ Any delays in the development, design and engineering of our products and services may adversely impact our business, financial condition and results of operations. Seasonality Risks ▪ There is a seasonal fluctuation in the need to fight forest fires based upon location. A significant portion of our total revenue currently occurs during the second and third quarters of the year due to the North American fire season, and the intensity of the fire season varies from year to year. As a result, our operating results may fluctuate significantly from quarter to quarter and from year to year. ▪ Extreme weather, drought and shifting climate patterns have intensified the challenges associated with many of the risks facing the Company, particularly wildfire management. ▪ The substantial majority of our revenue currently is concentrated in the Western United States. Sales and Customer Risks ▪ The aerial firefighting industry is expected to grow in the near future and is volatile, and if it does not develop, if it develops slower than we expect, if it develops in a manner that does not require use of our services, if it encounters negative publicity or if our solution does not drive commercial or governmental engagement, the growth of our business will be harmed. ▪ In the future, there may be other businesses who attempt to provide the services that we provide, or our main private competitors could attempt to increase operations. In the future, federal, state, and local governments and foreign governments may also decide to directly provide such services. ▪ If we experience harm to our reputation and brand, our business, financial condition and results of operations could be adversely affected. ▪ We have government customers, which subjects us to risks including early termination, audits, investigations, sanctions and penalties. We are also subject to regulations applicable to government contractors which increase our operating costs and if we fail to comply, could result in the termination of our contracts with government entities. 44

Risk Factors (3 of 5) Sales and Customer Risks (continued) ▪ The U.S. government’s budget deficit and the national debt, as well as any inability of the U.S. government to complete its budget process for any government fiscal year and consequently having to shut down or operate on funding levels equivalent to its prior fiscal year pursuant to a “continuing resolution,” could have an adverse impact on our business, financial condition, results of operations and cash flows. ▪ We depend significantly on U.S. government contracts, which often are only partially funded, subject to immediate termination, and heavily regulated and audited. The termination or failure to fund, or negative audit findings for, one or more of these contracts could have an adverse impact on our business, financial condition, results of operations and cash flows. ▪ We may be blocked from or limited in providing or offering our services in certain jurisdictions and may be required to modify our business model in those jurisdictions as a result. ▪ We may enter into firefighting contracts in the future with foreign governments, which may result in increased compliance and oversight risks and expenses. ▪ We may be unable to manage our future growth effectively, which could make it difficult to execute our business strategy. ▪ We rely on a few large customers for a majority of our business, and the loss of any of these customers, significant changes in the prices, marketing allowances or other important terms provided to any of these customers or adverse developments with respect to the financial condition of these customers could materially reduce our net income and operating results. ▪ Our cash flow and profitability could be reduced if expenditures are incurred prior to the final receipt of a contract. ▪ If we are not able to successfully enter into new markets and offer new services and enhance our existing offerings, our business, financial condition and results of operations could be adversely affected. Supplier Risks ▪ We rely on a limited number of suppliers for certain raw materials and supplied components. We may not be able to obtain sufficient raw materials or supplied components to meet our maintenance or operating needs or obtain such materials on favorable terms or at all, which could impair our ability to provide our services in a timely manner or increase our costs of services and maintenance. ▪ There is a limited supply of new CL-415EAF aircraft to purchase, and an inability to purchase additional CL-415EAF aircraft could impede our ability to increase our revenue and net income. ▪ We currently rely and will continue to rely on third-party partners to provide and store the parts and components required to service and maintain our aircrafts, and to supply critical components and systems, which exposes us to a number of risks and uncertainties outside our control. Disputes with our suppliers or the inability of our suppliers to perform, or our key suppliers to timely deliver our components, parts or services, could cause our services to be provided in an untimely or unsatisfactory manner. Legal and Regulatory Risks ▪ Our business is subject to a wide variety of additional extensive and evolving government laws and regulations. Failure to comply with such laws and regulations could have a material adverse effect on our business. ▪ Our operations are subject to various federal, state and local laws and regulations governing health and the environment. Financial and Capital Strategy Risks ▪ We may in the future invest significant resources in developing new offerings and exploring the application of our technologies for other uses and those opportunities may never materialize. ▪ We may require substantial additional funding to finance our operations and growth strategy, but adequate additional financing may not be available when we need it, on acceptable terms, or at all. ▪ Any acquisitions, partnerships or joint ventures that we enter into could disrupt our operations and have a material adverse effect on our business, financial condition and results of operations. As part of growing our business, we have and may make acquisitions. If we fail to successfully select, execute or integrate our acquisitions, then our business, results of operations and financial condition could be materially adversely affected, and our stock price could decline. ▪ Our systems, aircrafts, technologies and services and related equipment may have shorter useful lives than we anticipate. 45

Risk Factors (4 of 5) Financial and Capital Strategy Risks (continued) ▪ We have a substantial amount of debt and servicing future interests or principal payments may impair our ability to operate our business or require us to change our business strategy to accommodate the repayment of our debt. Our ability to operate our business is limited by certain agreements governing our debt, including restrictions on the use of the loan proceeds, operational and financial covenants, and restrictions on additional indebtedness. If we are unable to comply with the financial covenants or other terms of our debt agreements, we may become subject to cross-default or cross-acceleration provisions that could result in our debt being declared immediately due and payable. ▪ We do not expect to declare any dividends in the foreseeable future. ▪ Our projections in this proxy statement/prospectus rely in large part upon assumptions and analyses developed by us. If these assumptions or analyses prove to be incorrect, our actual operating results may be materially different from the forecasted results. ▪ Our variable interest entities (or “VIEs”) may subject us to potential conflicts of interest, and such arrangements may not be as effective as direct ownership with respect to our relationships with the VIEs, which could have a material adverse effect on our ability to effectively control the VIEs and receive economic benefits from them. Early Stage Company Risks ▪ We have incurred significant losses since inception, and we may not be able to achieve, maintain or increase profitability or positive cash flow. ▪ The requirements of being a public company may strain our resources, divert our management’s attention and affect our ability to attract and retain additional executive management and qualified board members. ▪ Our management team has limited experience managing a public company. ▪ If we do not develop and implement all required accounting practices and policies, we may be unable to provide the financial information required of a U.S. publicly traded company in a timely and reliable manner. ▪ Investors’ expectations of our performance relating to environmental, social and governance (“ESG”) factors and compliance with proposed SEC rules relating to climate change disclosures may impose additional costs and expose us to new risks. ▪ Pursuant to the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”), our independent registered public accounting firm will not be required to attest to the effectiveness of our internal control over financial reporting pursuant to Section 404 of the Sarbanes-Oxley Act for so long as we are an “emerging growth company.” ▪ We have identified material weaknesses in our internal control over financial reporting. If we are unable to maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results in a timely manner, which may adversely affect investor confidence in us and materially and adversely affect our business and operating results. Equity Risks ▪ The price of New PubCo common stock may fluctuate substantially and may not be sustained. ▪ New PubCo common stock is subject to restrictions on ownership by non-U.S. citizens, which could require divestiture by non-U.S. citizen stockholders and could have a negative impact on the transferability of our common stock, its liquidity and market value, and such restrictions may deter a potential change of control transaction. ▪ We may issue additional shares of common stock or other equity securities, which would dilute your ownership interest in us and may depress the market price of our common stock. ▪ We are an “emerging growth company” and a “smaller reporting company” within the meaning of the Securities Act, and if we take advantage of certain exemptions from disclosure requirements available to “emerging growth companies” or “smaller reporting companies,” this could make our securities less attractive to investors and may make it more difficult to compare our performance with other public companies. ▪ Provisions in our charter, Stockholder Agreement, and Delaware law may inhibit a takeover of us, which could limit the price investors might be willing to pay in the future for our common stock and could entrench management. ▪ If securities or industry analysts do not maintain coverage of us, if they change their recommendations regarding New PubCo common stock, or if our operating results do not meet their expectations, the New PubCo common stock price and trading volume could decline. ▪ There can be no assurance that we will be able to comply with the continued listing standards of the Nasdaq. The Nasdaq may delist our securities from trading on its exchange, which could limit investors’ ability to make transactions in our securities and subject us to additional trading restrictions. ▪ The holders of the New PubCo Series A preferred stock will have rights, preferences and privileges that are not held by, and are preferential to, the rights of holders of New PubCo common stock. We may be required, under certain circumstances, to repurchase the New PubCo Series A preferred stock for cash, and such obligations could adversely affect our liquidity and financial condition. 46